What would be your advice to someone building their nest egg?

Posted on August 16, 2019

My nephew Rob, age 25, asked me for some of my thoughts on investing. I gave him a few quick thoughts but then decided to describe what I think I’ve learned over the decades. This post is my advice to someone age 25. I would hope that Rob could be a self-reliant, highly efficient, and very successful investor. It’s not hard to do. Really! As I think about it, this advice is really for someone at any age who is building their nest egg. They’re in the save and invest phase. Not my spend and invest phase. Would this track with your thoughts?

== Imagine 8X. Even 16X. Save and Invest. ==

Why save and invest? Because when you store your savings in stocks you will build multiples more spending power in the future. Imagine: “What can I do with $1,000 now?” and ask, “Would I be happier if I had 8 times – maybe 16 times – this amount of spending power in the future?” This is a real choice because of the earning power of stocks and the power of compounding of returns.

== Think Real: avoid the distortion from inflation ==

We want to understand what happens to our money in real spending power. We make better financial choices when we think in terms of real return rates and real growth in future spending power.

Inflation shrinks the spending power of our money. The number of dollars we have today has less spending power than the same number of dollars we had in prior years. Inflation can lead us to conclude we are doing better than we really are. Inflation has a way to make the difference in return rates from stocks and bonds look less important than it really is.

== Store and build wealth in stocks ==

I can’t think of any investment that has a greater long-run return rate than stocks. Stocks average more than 7% real annual return. The next best, bonds, have averaged 3.1%. Your home – real estate – won’t increase in value much faster than inflation; after all, real estate is a component of the calculation for inflation. The value of homes Patti and I have owned increased by no more than 1% in real value per year when I adjust for inflation and all that we invested to improve them. Money market and bank savings accounts earn about 1% real return. Cash earns less than 0% because of inflation.

Stocks therefore are powerful earners and have 2.3X the real, long-term return rate of the next best alternative.

== Compound growth expands returns ==

Compound growth means you earn money on your original investment and on all the accumulated amounts in prior years. Small differences in annual return rates compound to big dollar differences in growth. The growth of stocks in one year is 2.3X that of bonds, but over time that difference expands to more than 6X.

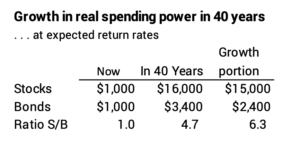

You can understand this by applying the Rule of 72. That Rule gives you a good estimate as to the number of years it takes for an investment to double. You divide the investment return rate into 72: an investment at 8% will double in 9 years. At a shade over 7% real return, an investment in stocks will double in spending power in 10 years. (That’s close enough.) At 3.1% real return, an investment in bonds – the next best alternative – will double in 23 years.

You have many years to let compound growth work its magic. Let’s assume 40. (Your life expectancy approaches 60!) For stocks that’s four doublings or 16X. Over that same period bonds will muster about 1.7 doublings and grow to about 3.4X. When you just look at the growth portion of the two, the difference is more dramatic.

== Tax-Fee Growth! You Can’t Beat It! ==

Tax-free growth is a wonderful thing. Always contribute to your retirement plan at work to get your employer’s match; that’s free money to you. Contribute more if you can to that retirement plan and to a Roth or Traditional IRA: $6,000 per year now. If you ever have a High Deductible Health Plan, contribute to a Health Savings Account: it’s the best ever.

== Investing Costs Cut. VERY DEEPLY. ==

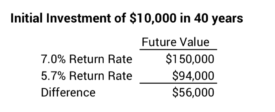

It’s this simple: do you want your investments to grow at a rate of, say, 7.0% or 5.7%? In this example below, would you rather have $56,000 more in spending power or not? Tough choice, eh? Most investors surprisingly choose the high cost option and earn at 5.7% giving up that $56,000. Huh? They don’t readily see and understand their investing costs (The financial industry doesn’t make it super clear.), and they don’t correctly think through the effect of high costs over ten, twenty, thirty or forty years.

We all incur investing costs. These costs are a net reduction from market returns. Investing costs are the sum of a fund’s Expense Ratio plus any fees you pay to a financial advisor. Ideally you are self-reliant and don’t incur advisor fees. Investors who incur fees from Actively Managed Funds pay roughly 1.4% of the value of their portfolio per year. That’s the direct reduction in their annual returns: 7.1% before costs less 1.4% = 5.7% net to you). Self-reliant investors no more than .10% (7.1% less .1% = 7.0% net to you). You will be hurt in the future – not do as well as you could have – if you fail to be an efficient, self-reliant investor. The good news is that it’s easy to be efficient and self-reliant.

== You can be in top 6% of all investors ==

You’ll be a winner when you predictably keep more of market returns. You keep more when you pay financial folks less. When you pay less you will be in the very top ranks of investors. The secret: only invest in broad-based, rock-bottom cost Index Funds. That’s easy to do today.

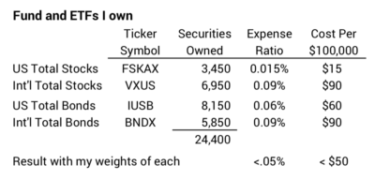

I own four Index Funds or ETFs equivalent to funds that in turn own a total of 24,400 securities – the great part of all the securities traded in the world. My total weighted investing cost is less than 5% of 1% of my total portfolio – .05%, and my costs have declined twice in the last year even though I didn’t change a thing in my portfolio.

Your chances to win are slim to none when you try to beat the market. That’s what Actively Managed funds try to do and basically why people hire financial advisors: they think those smart, hardworking folks can steer them to the funds that will earn more than market returns. It’s mathematically impossible for Actively Managed funds in aggregate to outperform Index Funds. Some funds do beat their peer index in a year, but over 10 years, it’s only about 6% who do, and it’s impossible to predict the future winners. You have more than a 40-year time horizon; that means it will be fewer than 6% who will outperform. You know you will be in the top 6% of all investors when you stick with index funds – and you’ll likely rank much higher than that.

I think the human brain is wired to tell us we can beat the market. We tell ourselves we are really smart, above average, and competitive. Investing in Index Funds means we are accepting that we will take a tiny bit less than what the market gives all investors and never beat the market. That just doesn’t fit who we are. I had to shift my thinking from “beating the market” to being a “champion investor” – focusing on how I likely will rank compared to other investors. Top 6% is good enough for me! That wasn’t an easy transition. It took me several years to get over my bad habit of investing in Actively Managed funds or taking flyers on stocks friends of mine would recommend. (Almost all those flyers were disasters.)

== You win by staying the course ==

Stocks and bonds have their ups and downs. Over your lifetime it is 99% certain that you will experience a year with -17% or worse return of stocks. Do not falter and change course. I invested $2,000 in a stock Index Fund in my IRA in 1982. It declined by 20% in one day (!) in 1987. It declined by -42% real return over three years starting in 2000. It declined by -36% return in 2008. When I sold that specific investment in January 2018 (in effect) it had grown 19.7X of that original spending power; that’s more than I’d calculate from the Rule of 72 (36 years would be 3.6 doublings and close to 12X) because the real return rate over that period was greater than 7% per year. (With inflation thrown in, my $2,000 turned into $102,800.)

== You just need to own four funds ==

You need no more than four Index Funds and you will own pieces of almost all the stocks and bonds in the world. That’s really all you need to do to be self-reliant and efficient. You saw the ones I own above. You can find these and similar funds or ETFs at Fidelity,Vanguard, Blackrock, or State Street.

== Use Holding Periods to set your mix ==

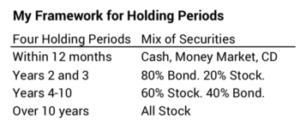

A Holding Period is the number of years you hold an investment before you sell it for cash to spend. Money you put in your IRA this year will likely sit there for 40 years before you sell securities for your spending. That’s a 40-year holding period. Stocks always outperform bonds by a wide margin for that length of time. That tells you what you should invest in: only stocks for that many years.

You will have other needs for spending with much shorter holding periods. You may have a need to save and invest to spend on a car four years from now. Or you want to save for a downpayment for a house. Those will clearly have short holding periods relative to your retirement accounts. In these cases you want to hold a mix of stocks and bonds. Bonds are insurance against the chance that stocks nosedive. When stocks have cratered – the ten worst years since 1926 average -27% real return – bonds don’t. You’ll be happier having held a bonds for short Holding Periods. You can see here that I annually take a snapshot of our portfolio arranged by Holding Period. Short holding period: mostly cash, money market, CDs or bonds. Long Holding Period: all stocks.

== Keep it Simple ==

Over time you want to keep your money in one place so you can keep it really simple as to what you own and how you are invested. Your accounts and holdings can get spread out and hard to follow with retirement plans from different employers and different kinds of IRAs. I have all my money at Fidelity. I like Fidelity’s web site and service. You cannot beat Fidelity’s cost for Index Funds.

Conclusion: You can be a winner in the top ranks of all investors. The first key is to Save and Invest as much as you can. You’ll most likely have 8X to 16X more in spending power from your investment in stocks in your retirement accounts, for example. The second key is to be Super-Efficient (and effective) by only investing in Index Funds: you only need to hold four. The third key is to Stay the Course: the value of your portfolio will vary; you’ll see periods of big downswings. But keep in mind that you have many years before you will need to sell any of it for your spending. You reduce uncertainty of the amount that will be there when you want to sell securities for your spending by estimating your spending needs by Holding Periods – how long you’ll hold on to an investment before you sell it. For short Holding Periods you’ll want mostly cash, CDs or bonds. Long Holding Periods should be all stocks.