Do you have the Rule of 72 drilled into your head?

Posted on September 21, 2018

I’m not sure when I learned about the Rule of 72, but it seems decades ago. It’s ingrained now. I also have “Ten years to double” in my head, which is derived from the Rule of 72. The purpose of this post is to explain the Rule of 72 and how I use it.

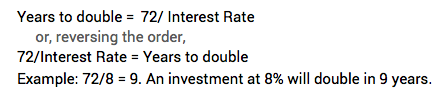

The Rule of 72 quickly conveys the power of compounding of investment returns. Here’s my most common use: “How many years does it take for an investment to double?” I’m surprised how many folks I ask, particularly younger folks, do not grasp this Rule. They have no idea how money saved now will grow over the decades. Here’s a short explanation of the Rule. You can explanations at Investopedia, Wikipedia, or here. Here’s my summary:

• The Rule of 72 is a shortcut to estimate the effect of compounding investment returns. I’m sure you remember the magic of compounding: every year’s growth is being computed on the original balance plus all the annual growth accrued from the beginning. Here’s the formula for the Rule:

I like to use the Rule of 72 with long term, average real investment return rates. Historically stocks have averaged about 7.1% real return per year. Bonds about 3.1%. (See here for these returns, corrected in September 2020.) What do those return rates mean for expected growth of a portfolio in the future?

1. Your investment in stocks at their expected return rate will double in spending power – every 10.1 years (72/7.1). Ten is close enough. I just use that.

2. Your investment in bonds at their expected return rate will double in spending power every 23 years (72/3.1). I wish it were closer to 20 or 25, since that would be easier to remember, but I’ll implant 23 into my brain.

========

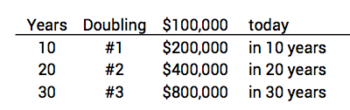

Younger folks need to focus on the ten. My niece is 35 and has more than $100,000 saved in her retirement plan. It’s all in stocks and she incurs virtually no investing cost (.02% in her Federal retirement plan!). She’ll most likely net very, very close to 7.1 % per year over her long, long investing horizon. How much might she have at age 65, 30 years from now? 30 years is three doublings or an 8X increase: $800,000 in today’s spending power. (That would be far more than 800,000 pieces of paper with $1 printed on each when one includes inflation.)

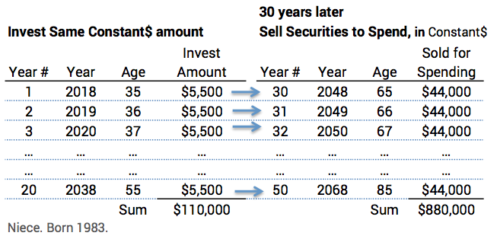

She also can get a much better sense of why it’s important to save and invest each year for retirement. Let’s assume she invests $5,500 into her IRA this year. All into stocks. She could think of her 2018 annual investment as the annual amount she would spend in the 30th year from now, 2048. How much would that be? That’s three doublings or 8 times $5,500: $44,000 in today’s spending power.

Let’s assume she repeats investing the same real amount each year for another 20 years (That would mean she adjusts the $5,500 invested this year upward for inflation each future year). She would have $44,000 in today’s spending power in the 30th year from now through the 50th year from now. She would be able to spend $44,000 (in today’s spending power) each year from age 65. This is in addition to her $800,000.

Of course, there’s variability in the 7% rate and the 3.1% rate. But over many years returns migrate to average close to those rates. (Surprisingly, statistically stocks migrate closer to their 7% rate than bonds migrate to their 3.1% rate.) Each 30-year sequence is going to be close to that 7% rate, and my neice in this example has 20 of those 30-year sequences to average. Those 20 will average out to be very, very close to 7% per year.

=========

We retirees don’t really use the Rule of 72 when we set our financial plan or think about it. We’re in the phase of Don’t Run Out. Our plan is built on the assumption that we will face the most horrible sequence of returns. The worst sequence we use for our plan is, in effect, below 0% cumulative return for both stocks and bonds.

I get most benefit of the Rule of 72 when I think about gifts to heirs or other family members. Patti and I really like gifts directly to IRA accounts and into 529 plans. I have in my head that each $1 gift now is much more valuable than $1. I think of each $1 gift as either $4 or $8 – because of the two or three doublings. In two cases for us, because of the young ages of the recipients, a $1 gift today is really $16 in spending power – four doublings.

Conclusion: The Rule of 72 is a useful shortcut to understand how many years an investment will double for a given investment rate. I use 7.1% as the expected real return rate for stocks. That translates to a doubling every 10.1 years. I use ten years for a doubling. I use 3.31% real return rate for bonds and 23 years for a doubling.

The Rule of 72 is most useful when I think of gifts to heirs or others in our family. A gift now is really much more in future spending power. Patti and I generally think of the gifts we make as either 4X or 8X the amount we give now.