Do you pay less tax on distributions from your Traditional IRA when you delay Social Security (SS)?

Posted on June 26, 2026

I’ve read this argument: delay the start of SS and distribute from your Traditional IRA because you will pay less tax on your distributions from Traditional. I did not consider the tax consideration in my post that recommends you start SS when you are ready. Now that I’ve thought through the tax implications, I definitely think you should NOT delay when you know you have enough for your spending that includes your SS. You pay more tax if you delay, not less.

You pay the same amount of tax on the amount you would normally distribute from your Traditional IRA before and after the start of SS. When you delay, you pay more tax on the increment you would distribute to get cash to replace SS; you pay less tax on the amount you would get from SS because a portion is tax-fee.

Details:

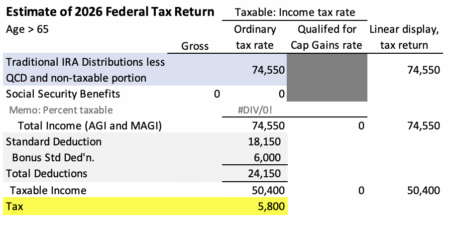

Base case: Let’s assume you are a single filer over age 65. Up to the first $74,550 of distributions from your Traditional IRA are low tax in 2026. That’s the amount of taxable ordinary income taxed to the top of the 12% bracket. None reaches the 22% marginal tax bracket. You pay tax of $5,800 or 7.8% of the $74,550.

That’s really a good deal. You avoided paying a much higher rate than this when you contributed; you are coming out WAY ahead in after-tax dollars for spending on difference in tax rates

== Start or Delay: example ==

Bob is 65. He is deciding whether or not to start SS at the start of his retirement – the start of his Spend and Invest phase of life.

Let’s assume Bob decides his Safe Spending Amount is $60,000 from his investment portfolio (see Chapter 2, Nest Egg Care), and all that will come from Bob’s Traditional IRA. If Bob has no other income, his total tax for 2026 would be $4,054: 6.8% of the $60,000.

Start SS. Bob adds the $35,000 he gets from from SS. His total for spending is $95,000. $5,250 of his SS is tax-free. (Income other than SS increases the percentage that is taxed; it reaches the maximum of 85% taxed when other income is roughly 1 1/2 times the SS benefit.) His taxable income is $89,750. His total tax is $9,669. He pays $5,619 tax on his $35,000 SS, an effective rate of 16%.

Delay SS. Bob decides to delay SS. He has to sell an added $35,000 from his Traditional IRA to get to the same $95,000 for his spending. All of that is taxable. Bob’s tax is $10,893. He pays $6,843 on his added $35,000, an effective tax rate of 19%. He pays $1,224 greater tax.

== Summary of two bad effects ==

• If Bob delays, he pays more tax, because he gives up the tax-free portion of SS. When his sells the added amount that equals his SS benefit, he has less net after taxes for spending. He has to make up that up by selling more than the $35,000 he would get from SS.

• If Bob delays, he increases his “sequence risk” – his chance of depleting his portfolio that he set in his original plan. He sells more securities for his spending than his calculation of what’s safe to spend. I use FIRECalc and find his $35,000 added spending from his portfolio chops off one year of NO CHANCE for depletion for one year delay. DON’T DO THAT.

Conclusion: I find no tax benefit for delaying the start of SS. I find the opposite: the added amount more that you distribute from your Traditional IRA to match the amount you would get from SS is taxed more than SS is taxed. You are selling more from your portfolio at the start of retirement than you have calculated is safe to spend: you are increasing your “sequence risk” – the chance of depleting your portfolio if you ride a most harmful sequence of stock and bond returns.