Why would you delay the start of Social Security (SS)?

Posted on April 17, 2026

The decision of when to start Social Security is a relatively small financial decision, but it can be a confusing one. The decision is straightforward if you’ve made the right decision as to how to invest your retirement portfolio. With two exceptions, you would NEVER DELAY the start of SS when you are retired. START now. The point where DELAY overtakes START is never less than age 85 and averages age +98 for the 96 months between age 62 and 70 that you could choose to delay. Your age to the breakeven point (BE) is greater than 95 for about 2/3 of the 96 months.

Details:

• It’s a small financial decision. In the example below, you are deciding whether or not to invest $3,000 to get $20 increase in SS for the rest of your life. I’ll assert your financial portfolio is $1 million. You are deciding how to invest 0.3% of it: small potatoes.

• The decision can be confusing because the number of months to breakeven (BE) – when DELAY overtakes START – is different for all 96 months between ages 62-70. And the number of months to BE is affected by the return rate you assume for your portfolio.

• The decision is clearcut if you’ve invested your retirement portfolio correctly. I would have assumed 6% real return on our retirement portfolio. I think you should that investment rate, too. You would NEVER decide to DELAY because your age to BE > 85 in all months and averages +98.

If I use a 5% real return rate, delay makes sense for nine months starting at age 64, but the cumulative benefit from delay for those nine months is small. The average age to breakeven is 89.

• Two exceptions favor DELAY: #1) those retirees with “more-than-enough” in their pre-tax IRA will want to delay to age 68; #2) a married, joint filer may want to delay (but never to age 70) if your SS benefit is greater than your spouse and your spouse is younger.

DEEP Dive:

== The BE calculation ==

How many months does it take $20 per month invested to overtake $3,000 invested?

Let’s assume you are 67+0 and your SS benefit at this Full Retirement Age is $3,000. Let’s imagine SS mails you a $3,000 check this month but offers you an added $20 per month for the rest of your life if you return it. You have two options:

1. Cash the check: START. You accept SS’s offer to pay you $3,000 per month in constant spending power for the rest of your life. You’ve got that $3,000 for your spending this month. You don’t have to sell $3,000 of securities to get that. You keep $3,000 more invested for the rest of your life.

2. Send the check back: DELAY. You sell securities from your investment portfolio to get the $3,000 for your spending. You have $3,000 less in your investment portfolio. Next month, SS will mail you a check for $3,020. If you cash that check, you get that added $20 per month in constant spending power for the rest of your life. You don’t have to sell from your investment portfolio for that added $20 each month for your spending. You keep each added $20 invested for the rest of your life.

At some point the $20 per month invested adds up to more than the $3,000 invested. We can calculate the months to BE. We add those months to your age and find your age to BE. If your age at BE is before your life-expectancy age, I argue that you should DELAY: you will have more at your life expectancy age.

== Months to BE change ==

SS offers a fixed monthly increase in three brackets from ages 62-64, 64-67 and 67-70. The offer for delay at the start of each bracket is a different percentage of your SS benefit at ages 62, 64, or 67. Those offers set the pattern of months to BE for each bracket. (See here for more detail.)

The months to BE increase every month in each of those brackets.

Example: next month you get a check for $3,020 but SS offers to add the same $20 per month if you DELAY again. You now are deciding whether or not to invest $3,020, not $3,000, to get a $20 per month increase. That’s at least one more month to BE ignoring the effect of investment returns. And you are one month older.

Example: You keep delaying. In 35 months at age 69+11, SS mails you check for $3,700 and offers an added $20 if you delay. You are deciding whether you should invest $3,700 to get a $20 per month increase. It will be many more months for the $20 to match the growth of $3,700 relative to the $3,000 when you were 67+0. And you are 35 months older.

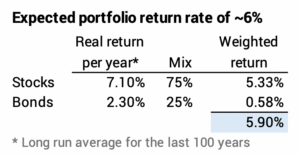

== Your expected portfolio return ==

Your expected portfolio return is real ~6% per year if you follow the recommendations as to how to invest in Nest Egg Care [NEC]. See Chapter 8. You’ll have no less than 75% stocks in your retirement portfolio. That’s also the default portfolio mix in FIRECalc. Patti and I started at 85% stocks for our investment portfolio and our investing cost is less than 0.03%; our expected real return was +6.3%; it’s turned out to be better than that since our start in 2014.

== Graph of age to BE: 6% real return ==

At 6% real return, your age to BE is more than 85 years for all 96 months for ages 62-70. It makes NO SENSE to delay in any of those months. The age to BE is > 95 in 65 of the 96 months. The average age to BE is 98.

(Your age to BE is below age 86 for two months; the amount extra that you’d have at age 86 from delay in those two months is less than $50 in today’s spending power; it’s the same amount you’d have if you spend 10¢ less per month starting at age 64.)

== Graph of age to BE: lower real return ==

I enclose the graph of age to BE with 5% real return. Your age to BE is less than age 85 in nine of the 96 months. You would delay those nine months starting at age 64+0, but I calculate the accrual of the benefit equal to an added $120 per year. That’s nice, but it’s trivial relative to what you spend in a year or will earn on your portfolio at your expected return rate.

That pattern repeats if you assume lower real portfolio returns. You find more months where age to BE is less than age 85. When you invest with a low expected portfolio return, you are buying a more complex decision.

== Exception #1: those with MUCHO ==

The big exception is for those who are retired and know they have “more than enough” for their spending in retirement. And they have a large pre-tax IRA that they know will eventually trigger IRMAA and might result in higher marginal tax rate from their RMD.

They may have been (should have been) on the march to convert as much of their pre-tax IRA to Roth. It is most tax efficient convert before you start on SS. About the first $20,000 converted in a year (single filer; $40,000 for married, joint filers) before SS is very low tax. After starting SS, that amount is not low tax because it triggers an increase in the percentage of SS that is taxed.

When I give this tax benefit to delay, I lop about 15 years for the age to BE. One would want to DELAY the start up to age 68.

== Exception #2: one has larger SS benefit ==

If you are a married, joint filer, your SS benefit may be much bigger than your spouse’s. Let’s assume your spouse is younger. You’d add more years to your life expectancy age to judge whether you should consider DELAY.

Example: At age 67+0, I had 18 years to my life expectancy of 85. Patti is three years younger and had 20 years to her life expectancy. If my benefit was greater than hers, I should add that five-year difference to my line on the graph for life expectancy. I should DELAY in months where BE age is less than 90 for me.

Conclusion: The decision of whether or not to delay the start of SS is a relatively small decision compared to decisions as to how you will invest your retirement portfolio. But it can be complex. The good news is that it is not complex if you have invested your retirement portfolio correctly: no less than 75% stocks and low investing cost (index funds). The decision is START now, since your age for DELAY to overtake START is never less than age 85 and averages 98 for all 96 months between age 62 to 70.

Exception #1: You should DELAY for all months up to age 68 if you are retired and on the march to convert pre-tax IRA to Roth to avoid the ills of future RMDs. You pay very low taxes on a portion of your distributions before you start SS. Your age to BE shrinks by about 15 years.

Exception #2: You may want to DELAY if your SS benefit is greater than your spouse and your spouse is younger.

Thank you! I’ve tried to explain this to other people over the years. I’m not sure why the prevailing “wisdom” is to wait as long as you can before taking SS. People say they want the higher payments, but I explain that if I take it at 62 instead of 70 I’ll get lower payments, but I’ll also get eight years of those lower payments! Heck, I may die in seven, and in that case get nothing if I waited til 70. People need to understand the breakeven point. Financial advisors need to do better!

Hi Tom.

I think folks don’t figure out what they really might earn on the money that they are keeping invested when they start SS early. I’ve seen explanations that assume 0%. Really low age to breakeven; in that case always delay. I see another that suggests using 2.3% as your investment rate in retirement – essentially 100% bond portfolio. Many ages where breakeven < age 85). Good news is that I'm darn sure you and I made the right decision, especially with returns over the last decade. But it is not an earthshaking mistake to delay. The decisions on 1) mix of S vs B and 2) investing costs (use index funds) are much BIGGER decisions.