“Why do I own bonds? The rate looks so low.”

Posted on March 2, 2018

My friend Betty asked that question and it’s a good one. The basic answer is that we own bonds as insurance to protect us from the DEVASTATION that BAD VARIABILITY of stocks returns would have on our portfolio. The returns from bonds are always greater (and almost always MUCH GREATER) than stocks when stocks tank. That’s when our insurance pays off: we sell mostly (or solely) bonds for our spending when stocks have tanked.

The purpose of this post is to describe the insurance value of holding bonds. You make your decision on how much insurance to buy (e.g., your mix of stocks and bonds) in Chapters 7 and 8 in Nest Egg Care.

We should always have stocks as the dominant portion of our portfolio. Stocks are the fuel for More-For-Us and our heirs when we ride other than a horrible sequence of returns. Bonds don’t have nearly the same power for More-For-Us. The average real return rate for stocks (about 6.4% per year) is 2.5 times that of bonds (2.6%).* That 3.8 percentage point difference accumulates to a BIG difference over time.

If we knew that the future sequence of returns we would ride would be average or even somewhat below average, it would be simple: never hold bonds. We see from history that we don’t need bonds at all for most of the sequences of returns we may face. For example, stocks have cumulatively increased by +15% in 75% of the three-year sequences of return (i.e., 1926 – 1928, 1927 – 1929, and so forth); that basically means most all of us** would Recalculate and find our Safe Spending Amount (SSA) would increase in all these cases; bonds would only depress those cumulative returns and lower the increase in our SSA (or the balance for our heirs if we chose not to increase spending).

But we don’t know the sequence of returns we will ride along. It’s a portion of the remaining 25% of sequences that are the concern – when stocks cumulatively decline in the first three years and then continue to decline. This is why we accept that 3.8 point average difference in returns by holding bonds. (See Chapter 8 Nest Egg Care.)

The BAD VARIABILITY of stocks is much worse than BAD VARIABILTY for bonds. The last post shows that when stocks tank, they really tank. Bonds also vary in return, but not as much as stocks. The statistical measure of variability (standard deviation) calculates that stocks are three times more variable than bonds for a one-year holding period. (A holding period is the length of time we hold on to a security before we sell it for spending.)

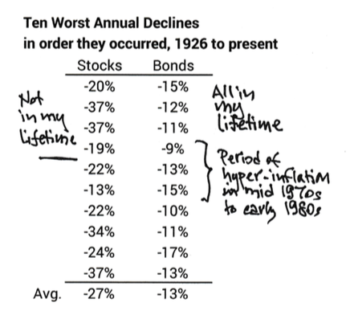

Here’s the table of the ten worst stock returns since 1926 in the order they occurred from the prior post, and I’ve added the 10 worst bond returns since 1926 in the order they occurred. (These are not for the same years.) You can see the 10 worst years for stocks averaged -27% while the ten worst for bonds averaged -13%.***

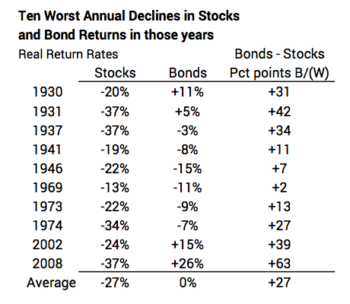

When stocks tank, bond returns have always been better – MUCH better on average. I lined up bond returns in the 10 worst years when stocks tanked. The table below shows that when stocks tanked, bonds outperformed on average by 27 percentage points. This is table shows why bonds are considered as a different asset class than stocks; when stocks zig, bonds can zag; or when stocks zig, bonds don’t zig as much.

We’re now seeing the insurance value of bonds. On average bonds cost us about 3.8 percentage points per year (the 6.4% less the 2.6%), but bonds pay us back seven times that on average that when we really need them. (Bonds paid off Big Time in 2002 and 2008, years when some of us may have been retired.)

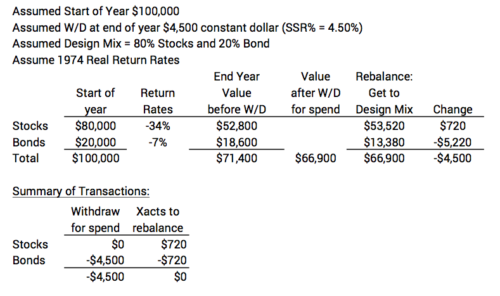

The math that requires us to rebalance our portfolio at the end of every year results in our selling mostly (or solely) bonds for our upcoming spending when stocks tank. You can follow this math in this example below. (You can see full size and print here.) This example shows that in 1974 (fourth worst year for stock returns) we would sell $4,500 for our upcoming spending from bonds and still have a transaction to sell $720 more bonds and buy $720 of (depressed) stocks to complete the rebalance task. We’re completely skipping selling stocks and giving them a chance to rebound. (Stocks did rebound in 1975: returns were +28% for stocks and +2% for bonds.)

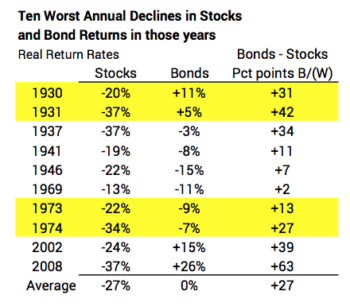

In our previous post, we found two back-to-back years of stock returns that appeared in many of the worst sequences of return: 1930 & 1931 and 1973 & 1974. I’ve highlighted those years. Bonds really helped in 1930 & 1931 but not nearly as much in 1973 & 1974.

We’re now starting to get a sense of the benefit of also holding a Reserve. I recommend a one-year off-the-top Reserve; we can use the Reserve for spending, and we avoid selling stocks or bonds in years that both have tanked. 1946, 1969 and 1974 would have been good examples when both stocks and bonds were in their worst 10% of annual returns. I’ll show the exact benefit of that action in future posts.

Conclusion. In years like 2017, we can conclude that bonds don’t do much for us and that they are costly in terms of lower total return. But we want bonds as insurance when stock returns tank. Bond returns are always better – most always MUCH BETTER – than stock returns when they tank. We get the benefit of holding bonds when we withdraw and rebalance for spending; we’re selling bonds, not stocks. We dodge locking in big losses. We’re giving stocks a chance to rebound to make our portfolio healthy.

* I take these returns from Stocks for the Long Run by Jeremy Siegel, Fifth edition. That was data though 2012. I get a greater real return rate for stocks and a lower real return rate for bonds when I extend the data through 2017. The differences would not change our thinking or decisions on the insurance value of bonds, so 6.4% for stocks and 2.6% for stocks is a good enough assumption.

** Not older retirees with Safe Spending Rates (SSR%) well in excess of 5%.

*** Data source for returns in this post: Stocks, Bonds, Bills and Inflation (SBBI) Yearbook, Ibbotson and Grabowski. The Yearbook has real annual returns for three types of bonds. I selected the returns from long term US Government Bonds for this post.