What is it that you HATE to spend?

Posted on March 22, 2019

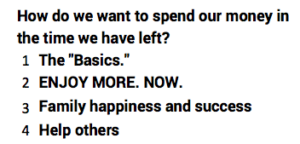

The last two posts (here and here.) discussed how Patti and I want to our spend money in the time we have left.

I then thought about our spending and made a list of where I dislike or even HATE to spend money. “Money equals value equals opportunities.” I need to prioritize the value I get from spending: I focus on large dollar expenditures. I don’t sweat the small stuff.

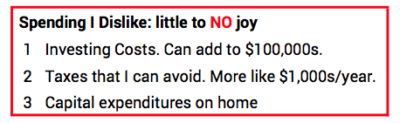

Each year I’m presented with opportunities to spend A LOT of money that I judge as REALLY LOW value: I don’t consider them as routine Basics; Patti and I get little or NO JOY from the spending; no Help now for our family; no Help to others. Here’s the list, and I’ll describe what it is I am doing about these expenditures.

== 1. Will NOT PAY normal Investing Costs ==

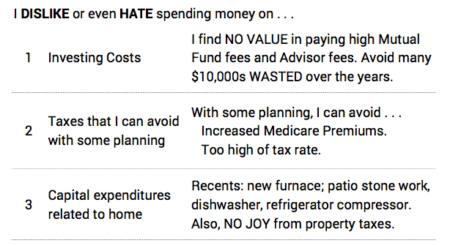

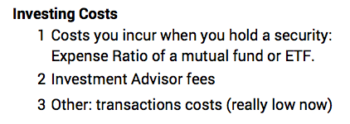

The top thing I DON’T WANT TO PAY is Investing Costs. I think the typical retiree pays out well over one percentage of their nest egg per year in these costs, while Patti and I are spending less than one-twentieth of that.

Every time you spend you are making a choice. Many retires choose the opportunity – the alternative – to pay high investing costs. Patti and I would get NO JOY from high investing costs. If we paid them, they would be the largest component of our Basics; they’d easily exceed all our utilities and cable TV, internet and phone. A cost of $10,000 per year will accumulate to several $100,000s in terms of lower value of your nest egg in time. I’d call that negative value from those costs. (See Chapter 6, Nest Egg Care or input different Investing Costs into FIRECalc.) Patti and I will always choose other opportunities – alternatives – that align with what we want to spend.

Patti may need some financial help if (when) I die first, (Recalculating her Safe Spending Amount (SSA); rebalancing her portfolio) but she’d be much better off to pay $400 per hour for what she needs than to pay normal fees based on Assets Under Management (AUM.)

== 2. Plan to Avoid taxes ==

I’ve mentioned these increases in taxes in recent posts (here and here). As nesteggers, we always plan for the worst; the assumption of horrible future financial returns drives our Safe Spending Rate (SSR%) to a low level. But at normal, expected returns for stocks and bonds, our retirement portfolio will continue to grow: the expected return rate for your retirement portfolio is greater than your RMD percentage for many years. Your portfolio will peak when you are in your early 80s. Your RMD percentage increases each year and therefore your RMD dollar amount will increase. At normal returns, it will be twice the amount you took in the year you turned 70½. In turn, this means two things:

1) You’ll have greater taxable income and continually get closer to income thresholds that trigger greater Medicare Premiums. Each threshold costs an individual about $1,000 per year. The first four thresholds add to $4,000 per individual. Double that for a couple who are both on Medicare.

2) Those with healthy retirement accounts when RMD kicks in at age 70½ can be pushed into the 32% tax bracket in future years. Some could find 40% of their total, lifetime retirement income taxed at 32%. UGH.

I have been oblivious to these potential increases in past years. I did a poor job of thinking about how to avoid these taxes. I’m going paying attention from here on out. We can avoid the impact of these two with proper planning. As I refine my planning process for 2019, I’ll keep you posted.

My general actions are clear: 1) convert some of my Traditional IRA to Roth; use Roth judiciously so I can spend more but not cross a Medicare Premium threshold; and 2) I’ll consider much higher donations to a donor advised charitable fund – prepaying future donations in effect. This action lowers the value of our retirement accounts; that lowers RMD and therefore the chance of getting hit with those higher taxes.

== 3. Pay some home costs differently ==

I’ve gnawed at these expenditures before, and this year I finally did something about it.

Over past several years, I’ve spent money to repair stonework on a patio, and we had to replace our furnace in December. Each of these cost more than $5,000. They were necessary (especially the furnace!), but I don’t consider these as part of our routine monthly spending for the Basics. They really were capital expenditures to maintain the value of our home, and Patti and I will never tap that value.

Patti and I also pay more than $5,000 of property taxes each year. These taxes add NO JOY.

As I think about the opportunity cost of these expenditures, in total they easily equal one trip to Europe per year for us. Is this the way we want to spend our FUN money? I think it’s fair to consider these two options; I use the furnace as the example:

1) Take the money from our annual Safe Spending Amount (SSA) and spend it on the furnace. That means we don’t take a trip to Europe that year. Or, since we don’t spend our total SSA in a year, spending it on the furnace means we won’t give gifts to family members’ retirement accounts; and the amount we gift this year may compound to a factor of perhaps eight (three doublings following the Rule of 72.

or

2) Pay those expenses from my Home Equity Line of Credit (HELOC). Pay monthly interest only. Never repay the loan. The principal is repaid on the sale of our home after we are dead. With inflation at 2% over the next decade, $10,000 now will shrink to about $7,500 in today’s spending power. That’s really a small nick off of the equity value that will be realized on the sale of our home after we are dead.

== Happy HELOC ==

I’ve had a Home Equity Line of Credit (HELOC) for a number of years. The loan balance at the end of December was $0. Last month I transferred an amount from the HELOC to our checking account equal to our recent capital improvements and this year’s property tax.

I’ll pay about $40/month in interest expense. That’s peanuts when compared to our SSA and other routine Basic expenses. The interest won’t be tax deductible because Patti and I will use the $27,000 standard deduction in calculating our taxable income. Also, interest from HELOC now is only deductible for capital expenditures for your home; I’ll keep track of the amounts that are for capital expenditures as distinct from property taxes in case we ever cross the $27,000 of deductible expenses.

Conclusion. We all have thoughts as to how we want to spend our money in the time we have left. I think it’s a good idea to think through priorities and write them down. Next, look at all that you spend. I think you’ll find some expenditures that just don’t align with the list of what you really want to spend. Patti and I will avoid Investing Costs like the plague: NO value (actually negative value) for us. We’ll use our HELOC for capital expenditures that maintain or improve the value of our home; we’ll pay back the loan principal after we are dead.