How much do you spend in a year?

Posted on June 24, 2022

I looked in detail at our spending in this blog about 18 months ago as a way to help me understand how much we needed to pay ourselves from our nest egg. I did the same exercise this week, but in a much simpler way. I just track the “Checks & Deductions” from our checking account to get the total that we spend for the past 12 months. This post describes how I did that.

== Why do I want to know? ==

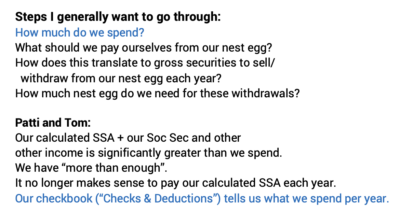

I want to know how much we spend in a year to know how much we need to pay ourselves from our nest egg. Patti and I are really settled in our spending habits. I don’t think our annual spending – measured in constant spending power – is going to change much the rest of our lives. We might have a bigger trip or extra trip in a year, but I think it’s more likely that we reach the point that we don’t travel as much. Once I have a good handle on what we spend now and will spend in a year, I can calculate how much total portfolio we need to have.

I do this exercise, because Patti and I have fallen into the category of having “more than enough.” (See Chapter 5, Nest Egg Care [NEC].) All nest eggers and many of those planning for retirement are in this category: returns have been excellent. We all have more now – even with this downturn – that we thought we would just a few years ago. We all have seen an increase in our Safe Spending Amount (SSA; Chapter 2, NEC.)

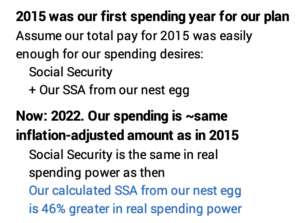

Returns for Patti and me since we took our first withdrawal for spending in 2015 have been such that our calculated SSA for 2022 is 46% greater in real spending power than for 2015. (That’s 76% when I add in inflation.) Our spending has not increased in real terms: we aren’t traveling more or more expensively, and travel clearly is our biggest discretionary expense.

If I pay 46% more from our nest egg, it will swamp our spending. It makes less and less sense to pay ourselves our annual SSA. It makes more and more sense to think of taking an amount off the top for significant gifts or donations: we don’t need to die with far, far more than we needed for our spending.

== What we spend: the simple way ==

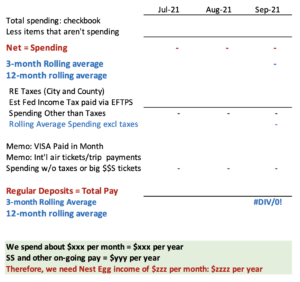

The simple way to figure out how much Patti and I spend is to look at our monthly checking account statements. I don’t spend from our Fidelity investment account; I only transfer our monthly SSA to our checking. The “Checks & Deductions” on my monthly checkbook statement includes all spending. I made this spreadsheet that you can download and entered the “Checks & Deductions” each month for the last year.

I want to exclude items I don’t consider as spending. Examples: I had an accumulated surplus (pay less spending) that I transferred back to my Fidelity investment account in December. I purchased an I-Bond in May; that hit my June checking account statement; that was an investment debited from our checking account.

I want to calculate the total spent over the last 12 months, but I saw three lumpy months that I wanted to understand before I just accepted the total as accurate.

1. Property taxes hit in my March bank statement. Big. Ugly. I get no joy by using our FUN money for property taxes. I always ask, “Why am I using our FUN MONEY to sink in a non-financial asset that that I’ll never get back in my life time?” I think I should use our HELOC to pay them, but I haven’t yet. Maybe next year!

2. Two credit card payments debited were roughly double the others. The big items are airline fares (At our age we fly business class for long trips.) and trip fees if we prepay all lodging and local transportation on an organized trip (Italy was the example last fall.) I can find those lumps by going on the internet and looking at the credit card statements, but I don’t have to do that since I use Quicken as our checkbook register. I have those items singled out in the detail of our credit card bill.

The lumps will always be there until I bit the bullet on those property taxes. They are part of our spending. But it was helpful to see that the on-going spending – excluding the lumps – is not that variable. That on-going spending is basically flat may be an obvious conclusion, but it was reassuring to see that. I see no pattern of increased on-going spending over this past year, although inflation has to be taking a toll.

This is step one of a process. Next week I’ll discuss the details of my thinking on the next steps.

Conclusion: I want to to understand how much we spend in a year. I think what we spend now won’t change much for the rest of our lives. The easy way for me to figure out how much we spend in a year is to add up “Checks & Deductions” for our last 12 bank statements. I can eliminate items that really aren’t spending. I can look for any unusual items in the months with lumps of added spending. In our case they are just lumps; we’ll incur similar lumps in the future. I found that our monthly spending, excluding the lumpy items, does not vary much at all. Maybe that’s an obvious conclusion, but it was reassuring to see that.

Understanding what you spend is key to understanding what you should pay yourself from your nest egg. And then you get to how much you really need in total portfolio value. I’ll get to my thinking on those steps next week.

My kids are available for your “more than enough” donations. They’ll spend your money like drunken sailors.