Have you written down your financial retirement plan?

Posted on April 30, 2021

I updated my summary of our financial retirement plan a couple of weeks ago. I show our original written plan in Appendix B in Nest Egg Care (NEC), and I displayed my summary 3 X 5 card from December 2014 on the last page of the Introduction in NEC. I’ve made no basic changes in six years, but my original 3 X 5 card was getting a little dog-eared and out of date. The purpose of this post is to show you my current 3 X 5 card summary of our financial retirement plan. Our plan is basically unchanged; I list the small tweaks that I’ve made in the past 6½ years. I suggest that every now and then you should review your written plan and update your summary 3 X 5 card.

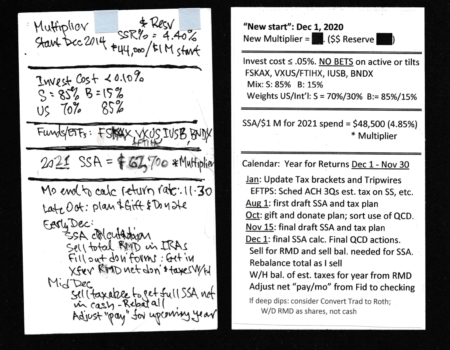

== My 3 X 5 card ==

I display my current 3 X 5 card and my new one. (I don’t show our Multiplier or the dollar amount of our Reserve; see Chapters 1 and 7, NEC.)

My new card is cleaner; I got fancy and typed it out. The top of my new card states that this is a “New Start.” That simply reflects the thinking in this post: all nest eggers earned back more in 2020 than we took out for our spending at the end of 2019. That means we all increased our Safe Spending Amount (SSA) for 2021 by more than inflation. We’re on a new path. (Most us also used a greater Safe Spending Rate (SSR%) from Exhibit D for that calculation.) (See Chapter 2, NEC for definitions of SSA and SSR%.)

== What has changed in the past six years? ==

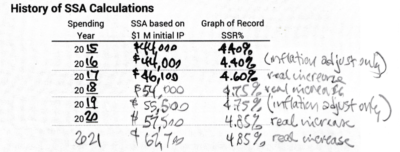

The basics are unchanged. Patti and I hold the same securities and in the same percentages (See Chapter 11, NEC.) I updated our Appendix B to show the history of our SSA. I show the detail calculations for all years in the post the first week of each December.

Some details changed. The biggest change is my annual tasks. I added tasks in late January and early August for tax planning. I’ve learned a lot about taxes over the last four years.

Here is the list of changes.

• The ticker symbol changed on the Total US Stock fund that Patti and I both own. Fidelity lowered the expense ratioon many of its index funds in 2018, and that led to changes in ticker symbols. FSKAX is the same fund that I display in Chapter 11, NEC (FSTVX), but its expense ratio is much lower – .015% or $150 per $1 million invested.

That lower expense ratio dropped our actual weighted expense ratio from 0.07% to a shade under 0.05% or $500 per $1 million invested.

• I now own two almost identical International Total Stock funds: VXUS (mostly) and FTIHX (some). I bought FTIHX(current ticker symbol for my original FTIPX) to simplify my annual rebalancing task. This is a small detail to save me maybe 30 minutes of effort when I rebalance each December!

• My list of yearly tasks is more detailed. The biggest change is that I spend time in early August to plan our taxable income for the year. I didn’t do that before. Why spend that time? With a bit of planning, I might avoid – as distinct from defer – a few $1,000 in tax the current tax year and maybe much more in the future. (Here’s my post on this task from last August.)

– I want to plan our donations for the year to use QCD because we always get the tax benefit of donations even if we take the Standard Deduction on our tax. When I use QCD I’m always getting the full tax benefit the donation. I would get no tax benefit if my Schedule A expenses, with our donations, added to less than the $27,700 Standard Deduction Patti and me for 2021.

– I want to estimate and maneuver our Taxable Income for the year for three reasons:

1) I take our total RMD in December and withhold A LOT of taxes to get to the total taxes we’ll pay for the year. We gain when I withhold almost all our Federal taxes for the year in December: I’ve gotten the interest-free use of tax dollars that I would have otherwise been paid earlier in the year; on average, that benefit is in the range of $1,000 per year. I also want to be accurate to avoid any penalties from withholding too little.

2) I want to possibly avoid a tax. The tax (in effect) that I want to avoid is a possible increase in Medicare Premiums. Medicare Premiums are deducted from our monthly Social Security benefits. The total premiums can increase based on prior year Taxable Income. The premiums increase when you cross thresholds of taxable income. If I didn’t plan and accidentally crossed a threshold by $1 of Taxable Income, Patti and I would pay an added $1,700 in added Medicare Premiums the following year. I don’t want to do that!!! This post shows the current thresholds.

I have some control over taxable income, since I have to decide what I will sell to get our total SSA for 2022 into cash by the end of this December. I can’t control the taxable income from RMD (Use of QCD helps.). But SSA is always greater than RMD: I have to decide what to sell in our taxable accounts – highest cost securities for lowest capital gains – or what to sell in my Roth account – no taxable income.

3) A small note at the bottom of my new card relates to longer term tax planning – beyond the current tax year. I need to think about the future tax bracket Patti and I might be in as our RMD grows. At expected returns for stocks and bonds, RMD could double over time. We could be pushed into a marginal tax bracket that I’d hate.

I can manage RMD two ways: 1) pay tax earlier at a lower rate now than I would pay in the future now by converting Traditional to Roth and 2) take my RMD when the market dips rather than on every December first: I will have a smaller amount in our Traditional IRAs and smaller future RMD than if I waited to take RMD until after the rebound.

Conclusion: I don’t look at my written plan, Appendix B in Nest Egg Care, very often. I’ve kept a 3 X 5 summary card on my desk in the cup with pens and pencils. I don’t look at that very often either, but I like that I have that short of a summary at my fingertips. I’ve had the same card for six years. I’d erase and replace a few numbers each December. It was looking dog-eared and wasn’t quite up to date. I describe my updated, neatly typed 3 X 5 card in this post. Not much has changed, but I did add a key task for tax planning every August.