How much does $2,000 saved and invested in 1985 translate to in 2021?

Posted on January 29, 2021

The purpose of this post is to tell the story that I repeat in my mind every January. I look back to see the impact of the money Patti and I saved and invested decades ago. The story this year is the $2,000 that I put in my IRA on January 1, 1985 compounded to $100,800 on the January 1 this year. (The $2,000 I invested in my IRA in the early 1980s is roughly the same spending power as $6,000 allowed now for IRA contributions.)

I’ve replayed this story for a number of years. You’ll find a similar post the last three Januarys. Here is this year’s story:

I invested $2,000 in my Traditional IRA on January 1, 1985; I was compulsive then about getting that money invested on the first possible day of the year. Conceptually I put that $2,000 in an envelope at the start of 1985, invested it solely in a stock index fund, and sealed the envelope and let it sit touched all those years with all dividends automatically reinvested. Patti and I open an envelope like this one each January 1 with great anticipation: we are sure that there is more than $2,000 in the envelope, but we don’t know exactly how much. We do know is that whatever is there is what Patti and I should FULLY spend in the year.

It was another really pleasant surprise this year: the envelope this year contained another fantastic gift in a series of really great gifts: we have +$100,000 to spend in 2021. The money in the envelope swelled 20 times in spending power. And there’s another gift envelope waiting for us next January!

(Note: in Nest Egg Care (NEC), we use a different and correct logic and steps to find what’s safe to spend in a year. We always assume we will face the MOST HORRIBLE sequence of market returns in the future. See Chapter 2. That assumption drives down the amount we judge as safe to spend from our total nest egg.)

== A series of annual gifts to the future you ==

Most people think they save for retirement with the goal of building a big nest egg. That’s good way to think about it, and clearly the amount you accumulate is the starting point for your financial retirement plan in Nest Egg Care.

But I think you should think differently when you are in the Save and Invest phase of life. You probably have a good guess as to how much spending – in today’s spending power – will make you happy in retirement. You want to think of the amount you save and invest this year as the amount that predictably – well, reasonably predictably – grows to what you want to be able to spend in a future year.

I certainly didn’t have this logic concretely in my mind when I was in my 30s saving and investing for retirement when I’d be in my 60s. But I did have the general concept that the money I saved and invested in the year I turned 30 would grow for decades.

Let’s assume I had this concept of a series of annual gifts to the older me. Let’s assumie I had a veiw that retirement was age 65 when I was 30. That would have meant the amount saved and invested that year year would sit there and then be spent in the year I turned 65. The money I saved and invested in the year I turned 31 would grow to an amount I would spend in the year I turned 66. And so on. In concept Patti and I have had a series of envelopes that we’ve opened and will continue to open each New Year’s Day well into our 90s: at some time in our 50s we stopped adding to our IRAs.

== The math of 12 times=

If you are in the Save and Invest phase of life, the amount you save and invest this YEAR could be the amount you have to spend each MONTH in a future year. That means the money you save this year grows 12 times in spending power. Admittedly this statement is based on a long time horizon like I used in the story Patti and I tell ourselves each year.

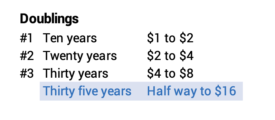

The math for 12 times comes from two numbers: 7.1% real return rate for stocks and the Rule of 72, which says stocks will double in real spending power roughly every ten years. (That 7.1%, less a bit of Expense Ratio, means your money doubles in real spending power a bit more than ten years, but “doubling in ten” years is a lot easier to remember.)

I use 36-year time horizon in each of my New Year’s Day envelopes – Jan 1, 1985 to December 31, 2020 for the one this January 1st. That’s roughly 3.5 decades and therefore 3.5 doublings. That mean the amount I saved in 1985 should have increased about 12X: 3 doublings are 8X, and five more years is roughly half the way to 16X. I then get a Rule of thumb for ~35 years: THE AMOUNT YOU SAVE THIS YEAR IS THE AMOUNT YOU CAN SPEND EACH MONTH IN A FUTURE YEAR.

== This year was better than 12X ==

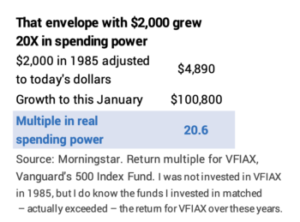

Is this how my $2,000 on January 1, 1985 worked out? Nope. BETTER. I have to adjust to inflation to get the change in spending power. From this CPI calculator, I find that my $2,000 then is the same as $4,900 in today spending power. Therefore, my multiple of spending power = 20 times. ($100,100/$4,900). The amount I saved in all of 1985 is money I can spend every ~2½ weeks in 2021.

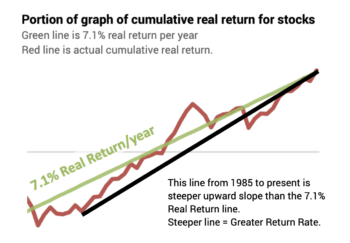

Why did this work out that way? Our returns depend on where the year falls on the graph of real cumulative returns over time. The 7.1% annual rate of return plots as a straight line on semi-log paper. If the year we invest is below the 7.1% line and our current year is on the line, the line from those two points is steeper than the 7.1% return line. Steeper upward slope = higher return rate. The line from early 1985 to the present is a steeper line. The 20 times over 36 years works out to average real return rate of 8.6%.

You can also interpret from the graph that includes bond returns that those who saved and invested in the early 1980s could hardly make a mistake with their investment. Bonds were waking from their ~45 years of zero percent cumulative real return, and any line for bonds in the early 1980s to the present is just as steep as it is for stocks – maybe steeper for some years.

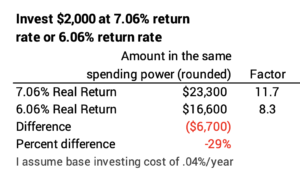

An investor could have made two mistakes: they could have invested in Actively Managed mutual funds that did not overcome their higher expense ratio; they could have invested in too narrow set of securities that did not keep pace with the market as a whole. One percentage point lower in return per year – the expected result from one percentage point of expense ratio, for example – would cumulate to about 30% less to spend now. $2,000 wouldn’t grow to $100,000. It would have grown to $70,000. $2,500 per month less to spend. OUCH: that is a big difference from something that most folks ignore.

== Lessons ==

• If you are in the Save and Invest phase of life, start saving for retirement EARLY. If you’re older and not in this phase of life, get your children and grandchildren to invest for their retirement. The EARLIER the BETTER. The MORE YEARS OF COMPOUNDING the BETTER.

• ONLY invest in stocks. NOTHING can compete with a 7.1% expected real per year over the many years you have until you will spend what you have invested. There will be periods that vary from that average, but your return from stocks is going to be very close to 7.1% over your lifetime.

• Think MULTIPLES of spending power. 7.1% per year compounds to ~doubling of real spending power in a decade. Decade after decade. $1 to $2. $2 to $4. And so on.

• Think that the amount you save and invest this year is a gift that you will spend in a future year. The money you save and invest THIS YEAR could be the amount you could spend PER MONTH in a future year.

• DO NOT GIVE UP ANY of the expected 7.1% away to high investing costs (Expense Ratio): only invest in total market index funds. (You’ll give up just a tiny bit of Expense Ratio.)

Conclusion. Each January I look back to judge the impact of the money Patti and I saved and invested many years ago. I invested $2,000 in my IRA at the first of January in 1985. I can view that as putting $2,000 in an envelope that has been invested solely in a stock index fund for 36 years. Patti and I opened that envelope on New Year’s Day and found it increased more than 20 times in spending power. (With inflation, the initial $2,000 I invested was more than $100,000 that we could spend in 2021.)

We don’t know future market returns. But the chances are that an amount saved and invested wisely this year will compound to MANY MULTIPLES of spending power. Save and Invest wisely if you are younger. If you are older, you can dramatically improve lives of those you love by helping them save and invest at a young age.