Do you want to buy an annuity to substitute for bonds in your portfolio?

Posted on September 3, 2021

You DO NOT want to buy an annuity to substitute for bonds in your portfolio! I read this article about a month ago, “Using Annuities During Retirement: When to consider annuities rather than bonds.” The article suggests that one should seriously consider buying an annuity rather than hold bonds because an annuity provides a larger stream of annual payments than the interest earned on a bond. The purpose of this post is to explain why I think YOU SHOULD NOT BUY AN ANNUITY to substitute for bonds in your portfolio.

== Why Bonds? INSURANCE ==

The article states that the primary benefit of an annuity rather than bonds is to provide a better stream of cash payments than the interest from bonds. This is the incorrect way to judge bonds. We don’t hold bonds in our retirement portfolio based on their potential for cash payments. WE BUY BONDS AS INSURANCE. We want to sell bonds when stocks crater, and stocks can really crater, and we can judge bonds by their ability to provide insurance – protect the value of our portfolio given that we retirees withdraw from it every year for our spending.

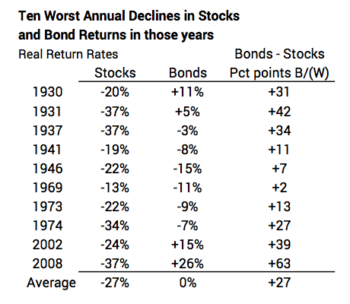

This post describes the value of bonds as insurance. Stocks outperform bonds by almost a factor of better than 2.5 times over the long run: stocks 7.1% real return and 2.6% for the average of intermediate+ long term bonds. If we could count on that every year, the decision as to what to hold would be EASY. But stocks don’t outperform in all years. Bonds have outperformed stocks in 28 of the 95 years since 1926. In the ten worst years where stocks have tanked, they averaged -27% real return while bonds in those years average 0% real return. Bonds outperformed stocks by an average of 27 percentage points in those years. And look at that most recent disaster for stocks in 2008. Wow! Now, that’s what I call INSURANCE.

== Where’s the insurance? ==

Let’s assume you decide on a mix of bonds 25% bonds and 75% stocks. (Patti and I are 85% stocks and 15% bonds.) Let’s follow the logic of annuities and assume you substitute annuities for ALL the bonds you would otherwise have in your portfolio. What’s that mean? You have a portfolio of 75% stocks in your brokerage account. That’s it. Stocks are only thing you can sell for your spending from your nest egg. When stocks crater, you have no bond insurance to tap. You are forced to sell stocks when they’re depressed. This makes NO SENSE to me. It makes no sense to give up any portion of what you consider as your bond portfolio – your insurance – for an annuity.

== How do they pay more than bond interest? ==

How do the companies selling you an annuity provide a greater payment stream than the interest from bonds? You think they’re doing something magical as to how they’re investing in bonds and they’re not. They invest mostly in stocks! The companies hold an investment portfolio very similar to the one you’d have with Nest Egg Care: let’s assume they settle on 75% stocks and 25% bonds. They use a Retirement Withdrawal Calculator similar to FIRECalc, to find the payout, somewhat analogous to your Safe Spending Amount. They then figure out how much they want to keep – a big chunk of it – and how they can dress up what they want to pay you to make it look attractive to the retiree fretting about low interest rates for bonds.

== The payout to you is low ==

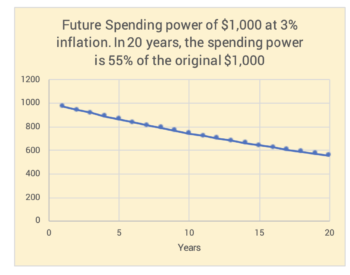

You will receive far LESS than you’d calculate for your Safe Spending Amount (SSA, Chapter 3, NEC) on the amount you’d pay for the annuity contract. The folks who sell annuities don’t pay out ANYTHING CLOSE to the spending power that you calculate as your SSA in NEC. Your SSA at least adjusts for inflation each year. They pay out a flat dollar amount per year. They can make that flat payout per year look attractive in the early years, because you’re absorbing the inevitable loss in spending power due to inflation. If inflation is 3% per year, You’ve lost 15% in spending power in about 5 years; 25% in 10 years; and your last payment of a 20-year annuity will have about 55% of the first-year spending power.

You get no benefit if stock and bond returns – what they’ve really invested in – are anywhere close to expected returns: 7.1% annual real return for stocks and 2.6% as the real return for the average of intermediate and long-term bonds. They have many annuity contracts spread over many years, and they know that they’ll average close too average returns over the years. But you’ll never see that.

What might you miss? Patti and I started with a payout for spending in 2015 of $44,000 per initial $1 million invested. Stock and bond returns have been above average over the last six year – and the look good so far this year – and our SSA payment on has in six years $62,700 for spending in 2021 – +43%. And it looks like we’re on track for another boost, greater than an adjustment for inflation. An annuity totally loses out on this potential.

You are giving them, unless you structure a death benefit or special features, the terminal value of your investment. Without special provisions that you pay for, you get no payout at the end of the annuity period and perhaps on death.

Graph 2-4 in NEC shows that at expected returns, a retiree who takes out 4.4% ($44,000 in constant spending power relative to $1 million initial portfolio) will have about 40% MORE in real spending power at the end of a retirement period than he or she started with; that assumes the mix assumption for the graph and average stock and bond returns. But even at poor future returns, one can see from the graph that a retiree will wind up with more than half of their initial portfolio’s spending power. Not zero. The obvious exception is the MOST HORRIBLE sequence of returns – the few chances out of 100 – that will eventually deplete a portfolio.

Conclusion. An article suggest retiree should consider buying an annuity contract for the bond portion of their retirement portfolio. This makes NO SENSE to me. The logic is incorrectly focuses on the annual payout of the annuity relative to interest received on bonds. We retirees don’t buy bonds in our retirement portfolio based on interest rates. We buy bonds as INSURANCE to protect us with stocks crater. We want to hold bonds to solely sell or disproportionately sell when stocks have cratered. We sell bonds to buy time for stocks to recover.

The economics of annuities are poor: they pay out far less than you’d calculate as your Safe Spending Amount, following the decisions you’d make for your plan following the steps in Nest Egg Care. Typically you’re giving up a significant terminal value that you’d like to pass on to your heirs.