What are my favorite productivity tools?

Posted on June 26, 2020

Why do I think about making my life more productive when I’m retired? I want to keep simplify the routine, take away stress, and try to be effective every day. I’ve mentioned a few of these before, but this post describes my checklist of things that I like. You might adopt a few.

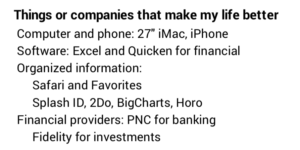

Hardware. I have an Apple iMac with a big screen – 27”. Someone advised me years ago, “Get the biggest screen you can afford,” and that was good advice. My bigger screen added $500 to my purchase last year. I kept my last iMac for seven years, and I may keep this one forever. (I’m hoping forever is more than seven years!) I look the extra cost as maybe $75 per year. Well worth it.

I switched to Macs decades ago. I find them intuitive and easy to use. I particularly like that it is very easy to organize files so I can find anything I’ve worked on. (I always put the month and day as the lead to every file name, so I can find it by remembering when I wrote it if all else fails. I stored the Word file for this post in a subject file for this week’s blog post, but the file name begins “0625,” the day I started on it.)

My friend David retired last year. He was a lawyer and didn’t use a computer much in his work(!). He purchased a portable PC after he retired. I’m sure the user interface has improved, but I’d hate to think of trying to get up to speed on that computer and screen size.

My iPhone syncs with my computer so all the bookmarks, etc. are the same. It’s a bigger screen, too. I read a lot on it, and it’s a helpful productivity tool.

My computer is in a room right off the kitchen. I’m usually close when I want to look up something but I’ve left my phone somewhere not convenient. (That’s more often than I like.) Or, I’ll be working on something and want coffee. That’s less than 15 feet away.

Software. I use Safari, Quicken, Excel, Word, Apple Mail and Calendar most often. I think I’d classify myself as an advanced user of Excel and Word. I’ve used both for decades.

== Quicken ==

My use of Quicken changed last year. I had to switch from Quicken 2007 for Mac. I likely paid $25 for it more than a decade ago. It was simple and clean. I HATED most all Quicken versions that were meant to replace it. Quicken announced they were no longer going to support Quicken 2007, and it won’t work on the most recent operating system for my iMac. I had to bite the bullet. Quicken Starter at $35 per year turned out to be a very good replacement – it’s far better than other versions that I tried. I don’t want the bells and whistles of more expensive versions.

Most of my friends don’t use Quicken or similar software to schedule or track their spending. I’d be lost without it. I have three checkbooks that I have to track: ours, one for a Trust set up by Patti’s brother (I’m trustee.), and one for a small non-profit that I co-founded. I need good information for the accountants who prepare the tax returns for each. But I’d want Quicken if it was just for our personal checkbook.

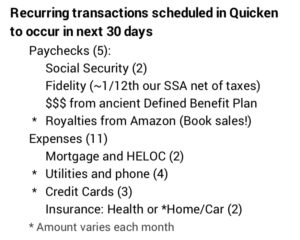

I particularly like the ability to schedule recurring deposits and payments and see what is coming in as paychecks and what’s going out as expenses for the next 30 days. I get a rough picture of our cash balance over the next 30 days.

I’ve set most all our routine vendors to ACH debit. I can’t be late in paying a routine bill and incur late fees or interest. Yesterday I got an email for the electric bill that will be deducted July 15; I entered that amount as a future payment; I can easily compare it to the payment of July 2019 to see if I think it is in line. Today I have 16 possible recurring transactions in the next 30 days; two are credit cards we rarely use.

I have a simple chart of accounts for our home spending that I set up years ago. Most all recurring transactions are already in categories, e.g., “Utilities”. The only bill with any complexity is our credit card bill; I have to detail the categories for important expenses to track, primarily those that could be tax deductible if we ever itemize.

I don’t use turbotax to prepare our tax return. I’m more than happy to turn that responsibility and drudgery over to someone else.

== Other Software ==

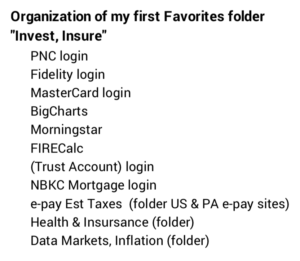

I like Safari and the Favorites bar in particular. My first Favorite is a folder labeled “Invest, Insure.” It has all the links to anything that has to do with money, insurance or health. I click on that folder and get quite a list. These sites and folders hold 90% of the sites I use in a year.

SplashID securely keeps all our important numbers: social security, checking accounts, investment accounts, credit cards, loans, numbers; VINs; insurance contracts; frequent flyer; other memberships. And many user names and passwords. I have 402 entries in my SplashID. Hmmm. I likely have some clutter in that that I should clean out; I’ll tackle that 10 minutes at a time – see below.

I use 2Do for reminders. I especially like my breakdown of the recurring series of small tasks I complete week by week in January and February to gather all the information for the tax returns. I dreaded this as one, complex task before. Not so now.

Banking, Investment Accounts and Information. I have the three checking accounts at PNC. I find its display of accounts is excellent. I use PNC’s BillPay for folks who can’t ACH our personal account. I haven’t written or printed a paper check to mail in the last 12 months. I deposit any paper checks we receive with mobile deposit. I rarely go into the big, beautiful bank building or its ATM.

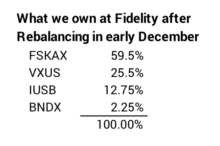

Our investments are in one place at Fidelity. Our account structure is simple. (See Nest Egg Care, Chapter 12.) I log on or Patti logs on and we both can see the total that we have. A friend of mine still has his investments scattered at many institutions and has never consolidated many retirement accounts from employers over the years. I don’t get it.

I find most folks who don’t keep it simple don’t know their mix of stocks vs. bonds, and that’s one of the four key decisions for any retirement plan. I think it’s impossible for them to rebalance at the end of each year.

Fidelity’s user interface and capabilities are terrific, but they should be comfortable to me since I’ve used the web site for many years. Maybe others are just as good, but I’d never change. I particularly like that I’ve linked our taxable account to our checking account and have automated our monthly “paychecks” from Fidelity.

I think I should be paying SOMETHING to Fidelity for the use of the web site, the tax reporting, and the free help whenever I call. I can even schedule a Zoom with Ryan, my assigned, no-fee advisor and fantastic information source if I ever get stumped. I only own one Fidelity security, FSKAX, and pay Fidelity a whopping $15 per $100,000 invested in FSKAX. (Expense ratio of .015%.) That adds up to very little compared to what I’m getting.

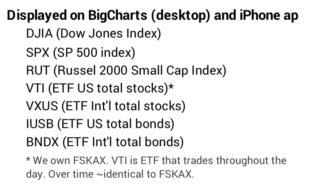

I’ve organized Big Charts for my desktop and the Stocks ap on my iPhone to track what’s happening during the day or at the end of the day. I can’t get away from checking at least once a day. Here’s the list of markets and securities that I see when I look at these two.

Other organizing tools. I like the clock function on my iPhone for alarms and the countdown timer in particular. I try to remember to use the countdown time when I pay for an hour of parking; I need to know when I have a few minutes left so I can use the Go Mobile PGH parking ap to extend my minutes. I HATE having to pay a $25 parking ticket because I forgot to extend my time for $.25. I messed up and paid two of those in 2019.

I added a simple countdown timer, Horo, for my desktop. I have two set timers, but can add more. One is for 10 minutes to work on tasks I really hate doing, like spending time to clean up the papers on my desk. Another is for 25 minutes to discipline myself to work uninterrupted on a project; I’m trying to use the Pomodoro Technique. My mind can wander and jump to something else too easily. As I write this, I see I have 13 minutes left on the current Pomodoro.

Conclusions. We all need to make our lives simpler when we are retired. I find the right hardware and software – computer and mobile phone – are important. For financial matters I rely on Quicken and Excel. I’ve automated most all monthly payments with ACH and BillPay at PNC. Our investment accounts are all at Fidelity and linked to our checking at PNC. I like my Favorites folder in Safari for all things “Invest, Insure”. SplashID is our secure place for important account numbers and logon information. I use a countdown timer many times a day. I’ve started to use the Pomodoro Technique. You may find some of these helpful.