Should Moncef Slaoui have sold his GlaxoSmithKline stock?

Posted on October 2, 2020

I read this article, “Trump’s Vaccine Czar Refuses to Give Up Stock in Drug Company involved in his Government Role”. The top scientist for Operation Warp Speed, Moncef Slaoui, was hired as a contractor, not as an employee, to avoid the ethics requirement that he sell stock holdings in a company that could benefit from his work. He said he didn’t want to sell his shares in GlaxoSmithKline (GSK) “because that’s my retirement.” This was $10 million in addition to $12 million stock he held in Moderna (MRNA) that he did agree to sell. What thought went into the decision not to sell GSK? Let’s forget the ethical issue about owning GSK: the purpose of this post is to look at what I think is faulty thinking – or perhaps not thinking at all – about a financial retirement plan.

Admittedly, $20 million or so is a VERY BIG net worth. It’s obviously hard to relate to, but I think the correct thinking Slaoui should have used would apply to any retirement portfolio: if I were Slaoui, I’d sell GSK in an instant.

== 50% of your nest egg in one stock? ==

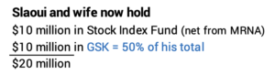

I’m sure I’m simplifying: I assume that Slaouis’ financial retirement plan starts now with total financial assets of $20 million. I’ll assume he netted $10 million on the sale of MRNA, and I’ll assume he put the net in a diversified index fund like FSKAX (I own), VTSAX or in an ETF such as VTI or ITOT. Terrific. But now he has $10 million in one stock. This would make GSK half of his financial next egg.

Would you hold 50% of your nest egg – or anything close to that – in one stock if you were thinking about a retirement? No! I realize the thought of paying taxes on gains far earlier than you otherwise would over the rest of your retirement plan would make your brain hurt. But that much in one stock means you’ve lost predictive power for your future financial returns, and that’s a Very Expensive loss in my mind.

You have predictive power – based on historical returns – when you own an index fund or ETF that reliably mirrors market returns. You lose predictive power from holding too much in one or several stocks. Will that one stock match, beat or underperform total market returns? You really don’t know. Keeping it adds too much uncertainty to your financial retirement plan. You never want to add uncertainty. You can’t trust any calculation of your Safe Spending Rate (SSR%). You can’t judge that your resulting annual Safe Spending Amount (SSA) is truly safe.

== A stock with lousy historical performance ==

The stock Slaoui will not sell is GlaxoSmithKline (GSK). GSK’s total return – the effect of stock price + dividends reinvested – lags the market – represented by a total market index fund – by about NINE percentage points per year. NINE! It’s lagged consistently over the last 10 years. This is SERIOUS under-performance. The worst stock mutual fund I can find – MUHLX, which ranks at the very bottom of all its peer funds in ten-year performance – is better in return than GSK.

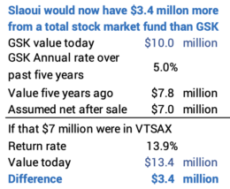

It’s not fair to use hindsight, but Slaoui would have $3.4 million more if he had sold his GSK five years ago. He has $10 million now, and I can work back in time using the return data to find he would have had about $7 million – net after taxes – five years ago. If he had then invested that $7 million in VTSAX, he’d have $13.4 million today. OUCH.

The past is a poor predictor of the future, but that poor performance makes it hard to conclude that GSK will match or outperform market in the future. If I were Slaoui, I’d sell it now. I’d have to override the discomfort of taking a tax hit now and selling well below it’s value at the start of year year. It’s the smart thing to do. This is very similar to the decision to hold onto a poor performing mutual fund or to sell it, pay taxes, net less, but grow with a market index fund. I describe that decision-process in this post.

== Is $45,000/month after taxes enough? ==

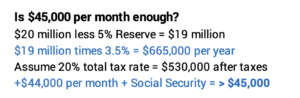

I’d bet Slaoui – or his financial advisor – didn’t spent five minutes thinking through how much $20 million delivers in terms of an annual Safe Spending Amount (SSA; see Chapter 2 Nest Egg Care [NEC]) for the balance of his and wife’s lives. In WORST CASE, starting now, his financial nest egg will deliver an annual SSA of $665,000 in today’s purchasing power for rest of their lives. Wow!

That’s pre-tax, so I’ll guess that is $530,000 after taxes that he and his wife have to spend or give away each year: that’s $44,000 per month. That doesn’t count the relatively small amount they’ll get from Social Security. The total is more than $45,000 per month. Can Slaoui possibly think that selling GSK – and paying tax on gains now – has a meaningful impact on his retirement?

I use 3.5% as the Safe Spending Rate (SSR%) for this calculation. I assume Slaoui and his wife start their retirement now. The article says she is 50 years old; her life expectancy is ~35 years. I only displayed SSR% up to 30 years in Graph 2-4 or the Appendix D Table in NEC. I use the same steps described in the text in Appendix D to find that that the SSR% for 35 years is 3.5%.

== Maybe it’s $90,000 – or more – per month ==

In a few years, their SSA will be almost certainly be more than $44,000 per month in real spending power. They’d start their plan now by withdrawing 3.5%. That’s less than 60% of the expected return on their portfolio – more than 6% – if they come anywhere close to the mix of stocks and bonds I recommend in NEC. It’s almost certain that they’ll earn back more than they take out in a year – or cumulatively in years – and they will calculate to a real increase SSA each time that happens. (See Chapter 9, NEC.)

How much might their SSA increase? I showed in this post that SSA for Patti and me would double in 20 years if future returns were average. It would be more than that for Slaoui and his wife. They start at a lower SSR%; its easier for them to reach the point when they calculate to a greater SSA; and they have at least another decade for their money to compound than Patti and I did at the start of our plan. But let’s just use that 100% – double – real increase in spending power. That’s ~$90,000 per month.

== Why donate all gains in GSK? ==

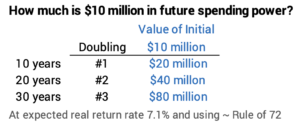

Slaoui said he would agree to donate all his future gains from GSK? Why do that? This makes no financial sense. That’s means he accepts NO potential future growth on $12 million for his retirement. Stocks double in real spending power every ten years at expected returns. It he sold GSK, he could see the net $10 million grow to $40 million in 20 years. (That’s two doublings; he’d be 81.) Or $80 million in 30 years. (That’s three doublings; his wife would be 80.) Who put pencil to paper to that?

Conclusion: Most folks don’t think about how to get their portfolio in shape at the time they start retirement and don’t figure out how much they will be able to safely pay themselves in retirement. This post discusses a set of decisions that did not make sense to me. My advice is: 1) Don’t own too much in a security or securities that add unpredictability to your future returns relative to market returns. 2) Especially sell securities where you think they could perform less than the market as a whole, regardless of today’s tax consequences. 3) Decide how much monthly “pay” you need in retirement – how much you want to withdraw from your portfolio that – along with Social Security or other income – will make you happy in retirement; you may find your nest egg now or in the near future will give you a very happy amount.