How does the second largest actively-managed fund – Fidelity Contrafund (FCNTX) – rank against its peers?

Posted on September 27, 2019

This post puts the second largest actively managed mutual fund – Fidelity® Contrafund® (FCNTX) – in the same barrel that I put American Funds Growth Fund of America (AGTHX) in two weeks ago. How well has FCNTX performed over the recent past compared to its peer index or a peer index fund? Basic answer: a lot better than AGTHX, but not as well as its peer index or peer index fund. Over the last decade, the annual return of FCNTX has lagged its peer index by about 1.5 percentage points per year.

== The glory days for Contrafund ==

In the two decades of the 1990s and 2000s Contrafund burnished Fidelity’s reputation for actively managed funds that outperformed almost all others. I pointed out in this post that that overall reputation for Fidelity has faded away: now very few of Fidelity’s actively-managed funds outperform their peer index, and none outperform close to the level that Contrafund did for 20 years.

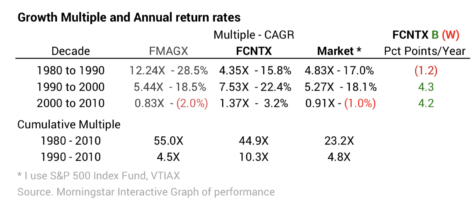

The most famous Fidelity fund is the actively-managed Magellan Fund (FMAGX). Its heyday was in the years prior to 1990 when its legendary manager, Peter Lynch, retired. For the decade before he retired Magellan was a rocket ship outperforming the market by more than 10 percentage points per year. Since then it has lagged. After 1990 Contrafund far outdistanced Magellan and the market for two decades: Contrafund beat the market by about 4 percentage points per year over 20 years. $10,000 invested in FCNTX in 1990 accumulated to more than twice that of the market as a whole by 2010.

[Full disclosure: I was an investor in Contrafund for many of its glory years. I sold my last shares to switch to only index funds in 2014 when I started our financial retirement plan following my advice in Nest Egg Care, Chapter 6.)

Fidelity tells me I’ve been a customer since 1984. I thought I was a customer earlier. I’m sure the $2,000 that I put in my IRA account at Fidelity each year for many years – starting no later than 1984 – was solely in Contrafund. That’s why I’m sure my IRA investments at least matched the strategy of holding a low cost index fund over the decades that I describe here.

I had a logic as to why I picked Contrafund: I concluded the only way to beat the market is to invest in a company judging that earnings and profitability will grow much greater than other investors – the market as a whole – expects. That’s a Contrarian Strategy: invest in companies that are out of favor with under-appreciated potential. If they deliver, performance is at a much higher level than expected. Stock price jumps to reflect the new expectations of future performance. I’d like to think I was very smart in picking FCNTX, but that’s just hindsight: one’s memory always places oneself in a good light. Likely reality is that I was just very lucky.]

Contrafund is a completely different fund from the 1990s. It’s a behemoth in terms of assets under management. It’s essentially limited to investing in companies with very large market capitalization values: it has to concentrate on the top companies in the S&P 500®. Companies at the top of market capitalization value today are clearly in the growth category. As I mentioned two weeks ago, that category – Large Cap Growth – has outperformed others in at least the last five years, and all funds in that category are going to look good relative to many other funds.

As an aside, Contrafund is an immensely profitable fund for Fidelity. It’s Expense Ratio – the money Fidelity gets – is now .82%. .82% * $85 billion = about $700 million per year! Wow!

== Recent Performance vs. the peer Benchmark ==

I use the same Morningstar (M*) data that I used two weeks ago to see how Contrafund has performed. I also include AGTHX for reference.

1) FCNTX against its peer Large Cap Growth index. This 10-year data shows FCNTX lags the index for Large Cap Growth by about 1.5 percentage points per year. The accumulated value from FCNTX would be about 15% less than the index.

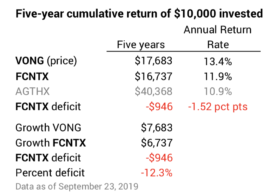

2) FCNTX against an index fund – actually an ETF – that attempts to mirror the Large Cap Growth index. I only have five-year data for that ETF: VONG. This is a better way to look at relative performance, since you could actually own that ETF rather than FCNTX. You see FCNTX lags VONG by 1.5 percentage points per year.

== Can FCNTX outperform in the future? ==

We don’t know but the evidence suggests that FCNTX will not outperform, and clearly that record of 4 percentage points better per year for many years looks impossible. Below I show FCNTX’s stock picking ability over the last decade. I add back the current .82% Expense Ratio for each of the past 10 years; that should be a pretty accurate apples-to-apples comparison to the index, which has no costs deducted. The table here shows no trend of FCNTX to outperform. An investor who paid .82% Expense Ratio per year – about 11% of the real, expected 7.1% growth for stocks – lost on that choice over the past decade and is losing this year so far.

Conclusion: Two actively managed funds dominate all others in terms of assets under management, AGTHX and FCNTX. This post looked at FCNTX’s performance over the last decade. FCNTX’s performance does not match its peer index or a peer index fund. Over the last five years it has lagged a peer index fund by about 1.5 percentage points per year. The stories of AGTHX and FCNTX confirms many other studies: funds that perform well over a time period just don’t sustain that performance over the long run. These two funds were top performers at one time. Money rushed in from new investors, changing the nature of these funds. Now they lag.