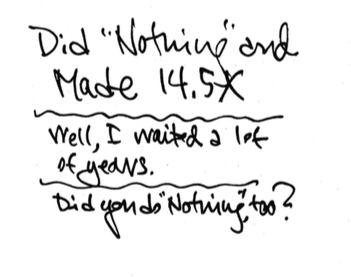

14.5X on my investment. Other Baby Boomers did that, too.

Posted on November 17, 2017

The game of Save and Invest that we retirees have played for decades has turned out to be a somewhat easy game. The timing has worked out great for us. We retirees have ridden an above sequence of annual returns for stocks. That’s added up BIG TIME for retirees who saved and chose the logical, simple way to invest.

Baby Boomers were born between 1945 and the early 1960s. Therefore, I’m about the oldest Baby Boomer. I’m using the example here of an investment made in 1981. I was 36 then. The youngest Baby Boomer would have been under 20, so he or she was not in the phase of Save and Invest then. So, maybe 1981 is applicable to folks who were at least in their late 20s in 1981 and could get serious about Save and Invest. Those are folks born in 1952 or earlier. They’re 65 or older now: that’s about 15% of our population; 48 million of us. Oh, if we Saved ANYTHING and Invested logically in 1981, we are very happy campers today.

IRAs that you could contribute to, separate from your employer’s retirement plan, started in 1981. You could contribute up to $2,000. You can contribute $5,500 now; that’s really the same inflation-adjusted amount of purchasing power as $2,000 in 1981. As it is now, the contribution was deductible from income for the calculation of Federal Income Tax. (That deduction is subject to certain income limits now and maybe then, too, but those never applied to me.) (Let’s forget in this discussion that I’m pretty sure I also invested that piece of taxes saved.)

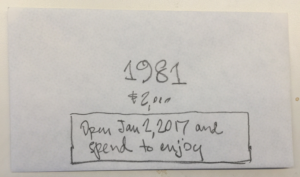

Did you contribute? I did. I was 36 in 1981. I’ve always been a saver and investor. A top priority every year was to first contribute to my IRA. In 1981 think I drove a nine-year old VW Beetle, purchased used. I got a $50 Earl Scheib paint job, so it actually looked pretty good. But I certainly wasn’t spending on a fancy car. Saving for my IRA was at the top of my list. I remember I was compulsive about writing a $2,000 check on about December 29 and mailing it on December 30 so it would be deposited and invested in my IRA on January 2.

I know how that $2,000 invested on January 2, 1981 turned out, since I made three good decisions.

The simple and obvious one was that it was always invested in stocks. My time horizon was going to be 30 years, maybe more, and for that length of time I knew stocks would outperform bonds and anything else I could consider in my IRA. Real stock returns have averaged about 6.4% over the past 90 or so years. That 6.4% translates to a doubling in purchasing power in every 11.25 years following the rule of 72. Over 30 years, I could have expected about 6.5X increase in purchasing power.

The second great choice was a mutual fund that closely matched what the market has given us over all those years. (I’ll get to my exact fund in a bit.) But let’s just assume I invested in a boring and dull Index Fund that, actually, because of its expense ratio, gave me a bit less than what the market would have given me without those costs. About the only one around at that time (Index funds first started in 1976.) was the Vanguard fund that tracked the S&P 500 index: VFINX.

The third best decision was that I did not change what I held all those years. I blithely blew right through some periods of very bad variability in stock returns. The real decline for stocks was about -14% in 1981, the first year out of the box. (I don’t remember regretting my investment that year.) The stock market declined by -22% in one day in 1987. Oh, my! The cumulative real decline for 2000, 2001, and 2002 was -42%, and who can forget the almost -39% real decline in 2008, the worst year in the history of the stock market dating back to 1802? Call it faith in the long run or inattention: I never changed what I held.

How did that turn out?

Let’s assume I put the $2,000 in an envelope on January 2, 1981 and wrote on it, “Open only on January 2, 2017 for your spending to enjoy that year.” (I think you have the idea that I have a series of envelopes like that.) How much was in that envelope when I opened it on this past January 2, 2017, 36 years later?

I can use the “Growth of 10K” graph at Morningstar.com to see how a starting investment $10,000 investment grew over any time period. (You enter the start and stop dates in the upper left hand corner on that graph.) I can then see how $10,000 invested grew. When I do that for my 36 years, I find VFINX went up 40X. That envelope contained $80,000 for spending to enjoy this year!

So, in real terms, I put in $5,500 of today’s purchasing power and had $80,000 for spending in 2017. That’s 14.5X in purchasing power. That means over that period I averaged a real return rate of 7.7%, not 6.4%. That was obviously a better than average 36-year sequence of returns. That’s the same stretch of stock returns all retirees experienced. The stock market has been very, very good to those of us who saved and invested in stocks in ways that most nearly matched what the market has given.

What’s in the next envelope that I will open this coming January 2 for spending in 2018? I put in $2,000 on January 2, 1982. When I open it on January 2, 2018, it would have traveled its own 36-year journey of returns. I can magically peer into the envelope using that same Morningstar graph. We’ll see what happens in the remaining weeks before January 2, but right now I can see $98,000 in that envelope! More than the 1981 envelope! An even better 36-year sequence! More Fun in 2018 than in 2017!

(I actually invested in FCNTX. I’m sure I picked FCNTX for a logical reason, so I’d like to think I was a very smart person to have picked it. But I now really think that it just turned out to be a lucky pick. You can use the same Morningstar “Growth of 10K” graph and see how that turned out. [I sold my last FCNTX in the fall of 2014 when Patti and I set our course for our Spend and Invest game, but my replacement investment that I mention in the book has performed close to FCTNX since then.])

Conclusions:

For those of us who saved many years ago and invested in stocks that simply mirrored what the market has given us, it’s been an amazing ride. We’ve been able to travel a favorable – above average – sequence of stock returns. Those returns and the effect of compounding over many years has meant many multiples of increase in purchasing power.

We retirees still have a long planning horizon. For most of us, it’s more than two decades. We have slices of our portfolio that we’ll hold for many years. Stocks will almost certainly outperform other alternatives for those slices, and (when we travel other than a horrible sequence of returns) almost certainly will result in multiples of their current purchasing power.

If you have heirs who would use your gift now to put into an IRA, as an example, the ultimate purchasing power of those gifts will almost certainly be many times your current gift.