What’s the chance you’ll see a real increase in your Safe Spending Amount in the next five years?

Posted on October 30, 2020

We nest-eggers always are spending – withdrawing for from our investment portfolio for spending – at a rate that equates to many years of ZERO CHANCE of depleting our portfolio. We always set a low spending rate because we assume that we always are facing the Most Horrible sequence of financial returns ever. It’s unlikely that we’ll experience the Most Horrible, but we clearly may face periods of poor returns. The purpose of this post is to answer two questions: What return rate on my portfolio will lead to a real increase in our Safe Spending Amount (SSA) in five years? And, roughly, what is the chance that we’ll experience returns at least as good that?

My answer is that Patti and I need about 10% real return on our portfolio over five years to result in a real increase in our SSA – an average of 2% return per year, and that’s less than one-third the expected return rate for our portfolio. It’s about 75% probable that we’ll earn at least that 10% over five years. That 10% return and 75% probability also apply to you assuming you follow the recommendations as to how to invest in Nest Egg Care.

== Why these questions ==

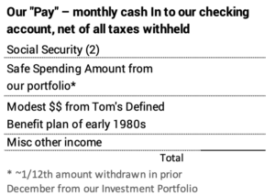

Patti and I are very happy with our monthly cash inflow to our checking account each month. Our SSA is +20% more than it was at the start of our plan. In a typical year – and clearly in a year like this where our spending on Fun Experiences is non-existent – we don’t spend our annual cash inflow to our checking account. We wind up giving the excess to our family or we donate more to charities.

Patti asked a couple of weeks ago, “How will I fare in the future when you’re not here?” (“Not here” means I’m dead!) I pointed out that she’ll lose my Social Security, for example, but the key thing that she WILL NOT LOSE is the amount that’s safe to withdraw each year from our portfolio.

Last week’s post said, “You will NEVER have a lower Safe Spending Amount than the one we have today; it will at least adjust for inflation, just like Social Security. The good news is that if returns match their long-run average, you can expect a 15% real increase every four or so years. Your total monthly pay will only get better. That’s +15% in four; +30% in eight; +50% in 12.

But I also wanted to give a different perspective. I wanted to find what kind of returns over five years would result in AT LEAST some real increase in our SSA – Patti’s SSA when I’m not here.

== The chance of an increase approaches 100% ==

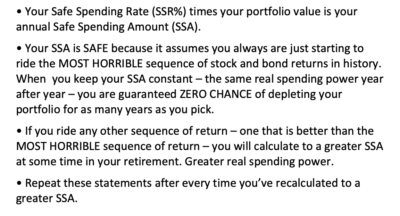

If I’ve done my job to explain how your SSA is calculated, you’ll understand that it is almost certain that you’ll calculate to a real increase in your SSA sometime during your retirement. You pick the number of years you want for ZERO CHANCE of depleting your portfolio. The only time you do NOT calculate to an increase in your SSA for those years is if you ride the MOST HORRIBLE sequence of returns in history. You’ll calculate a real increase in your SSA for all other sequences of return.

You may find that you’re are not riding the MOST HORRIBLE sequence of returns quickly. You may calculate to a real increase after your first year, or you may calculate to a real increase just one year before your final ZERO CHANCE year. The probability of calculating to some real increase is lowest at the end of year #1, and it increases to almost 100% when you near the years you chose.

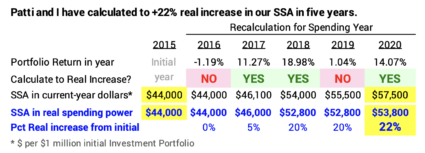

(Patti and I calculated to our first increase at the end of year #2, and we’ve calculated two more after that. Our total increase is +22% in real spending power. This is our calculation sheet from December 2019. The image is a brief summary.)

== The math ==

The math for the calculation to find what we have to earn for some real increase in our SSA in five years follows the same logic as last week’s post. We always calculate to a real increase in our SSA when we earn back in a year (or years) all that we’ve withdrawn for our spending – our total SSA withdrawn. We actually get a break on this: as we age, our Safe Spending Rate (SSR%) that we use for this calculation increases: we don’t quite have to earn back all we’ve withdrawn; we need less portfolio value for the same real SSA. We have to earn back less as the years pass.

== Our SSA will increase from 10% return ==

I calculate that Patti and I will calculate to some real increase in our SSA if we earn a shade more than 10% total on our portfolio over five years – 2% average annual return. That’s less than one-third the expected return on our portfolio.

This 10% return basically applies to you no matter your age. This is the same logic as I mentioned week. Younger folks with a lower initial SSR% will withdraw less over five years, but they get a modest benefit from increasing SSR%. Older folks – like Patti and me – start with a higher initial SSR% and withdraw more, but they get a bigger benefit from increasing SSR%.

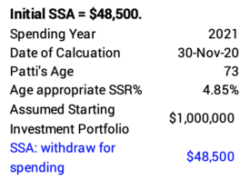

I’ve got to walk through steps to get to the 10% total return. My first step is to get the picture of our SSA in the first year. This assumes a starting Investment Portfolio of $1 million and uses the SSR% appropriate for Patti’s age this year. That’s $48,500.

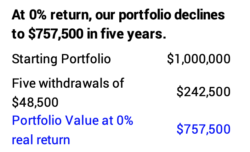

I use constant dollars – dollars in the same real spending power – for these calculations. With no real increase in SSA, the total withdrawn in the next five years would be $242,500. At 0% return over those years, that would deplete our Investment Portfolio to $757,500.

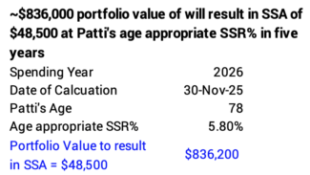

What portfolio value do I need in five years to calculate to an increase from the $48,500 SSA? I need to have a shade more than $836,200. The $836,200 is the break-even SSA of $48,500 divided by Patti’s age appropriate SSR% five years from now – 5.80%.

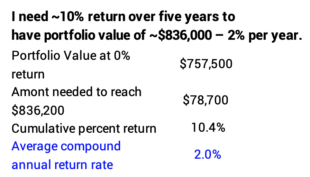

The last step is to find what cumulative return calculates to $836,200. I need a cumulative return of 10.4%: $78,700 on the $757,500 we would have at 0% return. This is 2.0% compound average annual return. The 2% annual return is less than one-third the expected 6.5% real return rate on our portfolio.

== We have 75% probability of increase ==

I conclude that it’s about 75% probable that our SSA will increase in spending power in five years. The converse is that it is 25% probable that five-year returns are not good enough to calculate to a real return in our SSA in five years.

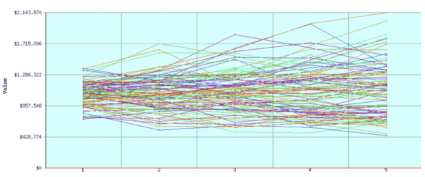

How do I get this 75% probability? I conclude this by looking at a graph of five-year returns from FIRECalc. I set FIRECalc to run all historical five-years return using a withdrawal of $48,500 per $1 million starting portfolio. I get a display of 90 five-year return periods or our mix of stocks and bonds. (I set the years to display as 1926 to present). Then, as best I can, I count those that are below the end point of $836,200 (~20) and therefore I know the number greater (~70). That means 70/90 or 78% of five-year returns will calculate to a real increase in our SSA for 2021 spending. Let’s call that 75% probability.

Conclusion: I found in this post that Patti and I will calculate to some increase in our annual Safe Spending Amount (SSA) in five years if we earn a bit more than 10% real return over five years: that’s an average of 2% per year – less than one-third our expected return rate for our portfolio. I also estimated that it’s 75% probable that we’ll earn at least 10%. I combine last week’s post. I have this sheet attached to our refrigerator now. It says:

The Safe Spending Amount (SSA), the amount that we will pay ourselves – or you will pay yourself if I’m not around – will NEVER be less than it is today. It retains its same spending power over time, because it adjusts for inflation just like Social Security.

This is a guarantee for the years equalt to your expected lifetime – the nest 15 years to your age 88 and my age 91.

Our SSA almost certainly will be better – we’ll be albe to increase it to more spending power.

If returns match their long-term average return rates – we can expect a 15% real increase in our SSA every four or so years. That’s 15% more spending power in four; +30% in eight; and +50% in 12.

Even if returns are not that good – just one-third of what we should expect for our portfolio – we have a good chance to calculate to some real increase in our SSA every five years.

We’ve planned for the worst, but it is most likely that our ability to spend – your ability to spend if I’m not around –will be much better in the future.