What are the basic steps to rebalance your portfolio?

Posted on July 10, 2020

Ages ago – over a year ago, I think – the links broke under the Resources tab on this web site. Nothing downloaded when you clicked on the resource. Reader Jeff asked me for replacements. I emailed them to him after I had updated a few. I got the links fixed, but, shame on me, I never added the updates to the web site. The purpose of this post is to simply inform you: I posted in the Resources section my latest spreadsheet to help for your annual Rebalancing task. I think it’s simpler to understand than the one I had there before.

== Why Rebalance? ==

You Rebalance your portfolio once a year to get back to your design Mix of Stocks and Bonds. (See Chapter 8, Nest Egg Care.) Throughout the years – not every year – you will be selling stocks to buy bonds as your final rebalancing task. That’s because over time stocks outperform bonds. Bonds are basically insurance from having to sell stocks in a year when they’ve cratered. Bonds have performed better that stocks in all of really bad years for stocks. You can also think of it this way: you are selling solely or disportionately more bonds than stocks to give stocks time to recover.

== Rebalancing: not like falling off a log ==

I struggled when I first tackled the task to Rebalance. I thought this was trivial math and steps. It was a bit of a struggle to get the hang of it. Follow the spreadsheet, and it will be a lot easier for you than it was for me when I first started to figure out how do this. You are essentially selling securities from your portfolio in a way that rebalances your portfolio.

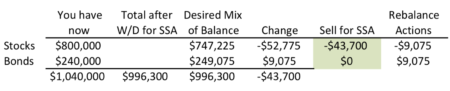

The simple key for the Rebalancing task is to first subtract your withdrawal for your upcoming spending in the year – your annual Safe Spending Amount (SSA; Chapter 2, Nest Egg Care) and then rebalance the remainder. I think you get the picture of this logic in the display here (The SSA withdrawal is $43,700.), but you can follow the detail I describe for this example in the spreadsheet.

As the last step – or near the last step – you decide how much Stocks or Bonds to sell for your SSA. After you sell, you still may have transactions to get to your desired Mix of Stocks and Bonds.

Conclusion: You’ve decided the total that you want to sell from your portfolio for your spending in the upcoming year – typically your your your Safe Spending Amount (SSA). After you’ve your withdrawn your SSA, you should Rebalance your portfolio to your Mix (Stocks vs. Bonds) and Weights (US vs. International) that you set at the start of your plan. Rebalancing may be easy to describe, but it was a bit confusing for me for a couple of years. My advice is to use the spreadsheet I provide here and in Resources to help you with this task.