Is your checkbook Neat or Sloppy?

Posted on April 19, 2019

I guess I would judge mine as both Neat and Sloppy. I think it’s always been both Neat and Sloppy. But what’s Neat and what’s Sloppy have switched over time. This post describes what I mean. Is your checkbook Neat and Sloppy? You actually want it to be sloppy in the same way that ours is sloppy! You’ll be happier!

== Years ago: Neat and Sloppy ==

Neat. Years ago my checkbook was Neat because I managed to never have much excess cash sitting there un-invested. Maybe Efficient is a better word than Neat. I was relentless in getting money invested as quickly as possible. I worked hard to avoid earning 0% real return on idle cash in checking. (The real return on idle cash was worse than -10% in years of high inflation in the late 1970s and early 1980s.)

I received a printed paycheck every other Friday. I went to the bank to deposit it during lunch hour. I had estimated the amount that would be excess in checking – sometimes I did not need all from my paycheck for expenses in the upcoming two weeks. I wrote a check for the excess to one of my funds at Fidelity and mailed it that same day. Fidelity cashed the check and invested the proceeds on the following Monday or Tuesday.

Did this make sense? Well, if that meant I had an extra $1,000 invested for one year, say in the early 1980s, and kept it invested, that $1,000 would have compounded to a healthy multiple: you can see the example of a +40X multiple here.

Sloppy. My recording of checks that we wrote and reconciling our checkbook with the bank statement was sloppy. I’d forget to record a check; Patti might fail to tell me about a check she wrote; I’d make errors in recording the amount of a check; I’d add or subtract incorrectly. The end-of-month reconciliation drove me CRAZY. I got very lax, and I think I’d go months without a detailed reconciliation. That caused more pain later in the year. Sloppy, sloppy, sloppy.

== Now: Neat and Sloppy ==

Neat. My checkbook records are VERY Neat now. Two things make my records meticulous.

#1. I don’t remember when I bought our first PC, but I started using Quicken shortly thereafter. My current records in Quicken stretch back to before 2000. I’ve entered every check and balanced our accounts every month for years now.

Quicken automates recording of deposits and bills. I have 43 Scheduled Transactions that enter automatically; they repeat either monthly, quarterly or annually. (Twelve are for quarterly estimated taxes: Fed, State and City.) Some have the same dollar amount for each entry in a year (e.g., Tom’s SS Deposit). I have to enter the dollar amount for some each time (e.g., electric bill; annual home owners insurance).

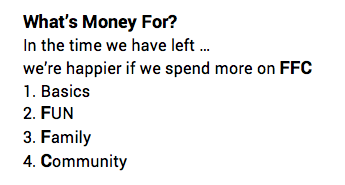

I have a very simple chart of accounts. I code major expenses (e.g., health insurance; medical expenses) and expenses on our credit card (e.g., Donation, Travel/Vacation) so I know potentially tax-deductible expenses and other expenses. I can easily run a report and add up what we spend on the Basics and what we spend on Fun, Family, and Community.

#2. Online banking has made bill payment and maintaining an accurate checkbook so much easier. I really like PNC’s online banking and its mobile app.

I’ve allowed vendors to debit our checking account for all our routine bills (e.g., utilities, insurances, MasterCard). I use online banking to enter the checks that PNC will print, put in an envelope, add postage, and mail. I have about 20 routine or past vendors stored in Bill-Pay. I’m shooting to write fewer than 20 handwritten checks that I have to mail this year. I’ve handwritten six so far this year.

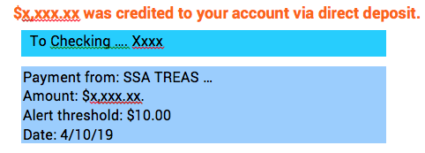

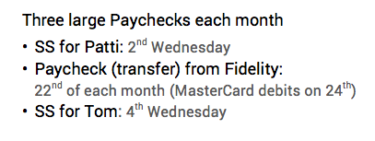

Online banking lets me set alerts. I’ve set it to email me when our three paychecks have been deposited: Social Security for each of us and the monthly transfer from our Fidelity investment account. I made pncalerts@pnc.com a VIP on my iPhone so I get a notification on my lock screen when the email arrives telling me those have been deposited. I get a little shot of happiness when I look at the message on my screen telling me that money is rolling in. (I don’t want to know when someone is taking money from our account: no alerts for that!)

I’m sure I spend more time with Quicken and online banking than I did years ago, but now it’s short bursts of time. I might spend a few minutes to make sure I have entered the correct amounts for recent bills and deposits into Quicken or to enter a payment to a vendor who does not debit our account. Reconciling my Quicken record to the bank statement takes less than ten minutes.

Sloppy. I carry an average checkbook balance that would have driven me wild ten or more years ago. I auto-transfer our annual Safe Spending Amount as a paycheck, in essence, from our investment account at Fidelity. I’ve timed that payday to ensure that I ALWAYS have enough to fully paying our credit card bill.

How large is our monthly balance? Large. I can see this three ways. One way is to go online and look at the stated average monthly balance for each statement. Right on the first page I see “Average Collected Balance for APYE” – that’s the amount PNC will use to calculate the interest they will pay. As I click through the statements in 2018, I see the average balance never fell below than one month of pay as a reserve.

I can also click on tab for “Daily Balance Detail” for any month and find the low spots in a year: I had three low spots (April, May and June) in 2018 that lasted no more than a few days each, and they really weren’t that low. The staggered timing of our paydays throughout the month wiped out these low spots. (It’s also low at the end of December – as planned – when I spend or gift the last of our SSA for the calendar year.)

The final way is to look at the interest I earned on my checking account for 2018. PNC pays .01% interest on my checkbook balance (Wowee!). For all of 2018, I earned more than $1 of interest, meaning my average daily balance was in excess of $10,000.

== Rationalizing my Sloppiness ==

I can look at my sloppiness of a high checkbook balance in the context of my complete investment plan. My game to maximize future returns for Patti and me – obviously with the constraint of never spending more than our calculated Safe Spending Amount – is based on two decisions: 1) our decision for our mix of stocks and bonds – 85% stocks and 2) our rock-bottom investing cost – less than .05%. Years ago I would have had a high mix of stocks, but I had more than 150X greater investing cost. (That was a mistake!) I now give up $tens per month earning potential from our high checkbook balance, but I gain $hundreds from the lower investing cost.

The other way to look at it is that I’m happy to give $tens per month because a large balance in our checking orients my brain correctly. I like the pressure it places on us: “You and Patti have plenty just sitting in checking to spend to enjoy. Remember: you don’t have an infinite amount of time to enjoy it. Figure out what you are going to do to Enjoy and do it NOW.

Conclusion: My view of what’s efficient and effective in managing our money has changed over time. Patti and I carry a much larger balance in our checking account than I would have tolerated years ago. If I view that as part of our whole investment plan, it’s a small inefficiency from essentially no return relative to the big efficiency we’ve gained from dramatically lower Investing Cost. I like the pressure from a high balance in our checking account: it forces us to think how we are going to best spend it for Fun, Family, and Community.