Is this a good time to retire?

Posted on November 20, 2020

Is this a good time to retire? Is this a good time to be retired? I’d say YES and YES. (I’m ignoring Covid-19, of course.) Two reasons: 1) Covid-19 has shut us all down: our spending is down to the basics. We’ve been shut down, and we all know the spending beyond the basics that will make us happy. 2) Your financial portfolio has NEVER BEEN BETTER in your life. The purpose of this post is to discuss why you should feel pretty good about retirement now.

== Your spending has crashed ==

The fact that your spending has crashed is not all bad. You don’t have much to spend on other than the basics. If you didn’t know what you spent on the basics before, you should know now. I dove into the details of our basics last month.

I see that effect in our checking account. It is really is SWOLLEN and it will get bigger by the end of the year. I’ve continued to pay our monthly SSA for 2020 from our investment account at Fidelity to our checking account, but due to another refund of airfares, I won’t pay a credit card bill this month or next.

== What spending makes you happy? ==

We have been forced to think about what it is that we really miss. For Patti and me it’s time with family and friends and travel. US travel and visits with family and friends don’t cost much. The things that cost are the experiences Patti and I like to buy – international travel. We really missed our annual walking trip to England this year, and we know we want to go back. We’ve never been to Tuscany, and we had a great trip planned that we put on hold. I’m anticipating taking those trips BIG TIME. My friend Betty says we should add Japan and New Zealand to our bucket list.

I’m optimistic about the vaccines. Given our ages, we should be in the first 20 to 30 million or so to be vaccinated. If we’re vaccinated by late spring, we might be able re-create some our 2020 travel plans in 2021. I’d guess that we’ll be short on spending on experiences in 2021.

== The big burst of growth ==

• If you were nervous about starting out in retirement, you should be A LOT LESS concerned now. You have more money now than you ever had in your life; the US stock market peak was earlier this week. If you had a Safe Spending Amount in mind that would make you happy in retirement, I’d guess you are there now: returns and growth of your portfolio have been terrific.

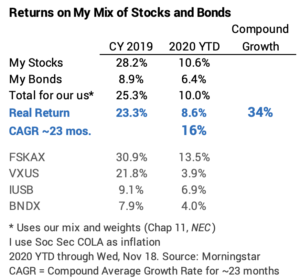

I’m amazed at how this year seems to turning out for both the stock and bond returns. Returns in 2019 were outstanding and they’ve been excellent so far this year. The expected real return for my portfolio is 6.5% per year, and our return has averaged ~16% per year over the past ~23 months. You should be very close to those returns and have a portfolio with +33% in more in real spending power than you had just two years ago.

That added portfolio value directly translates directly to 33% more in your annual Safe Spending Amount (SSA, Chapter 2 Nest Egg Care). Example: If you had $1 million two years ago and you thought your SSR% would be 4.4% in two years when you’d retire, you likely were planning that you could spend $44,000 from your nest egg. Now with 33% more, you can spend $58,000 – $14,000 in more spending power per year for the rest of your retirement. That’s a BIG BOOST in happiness.

• If you’ve been retired, you have to be ecstatic with what’s happened to your SSA and your portfolio over the last four years. You’ve experienced what Patti and I have experienced. Your SSA has increased by roughly +25% in real spending power. That’s true no matter your age and no matter your mix of stocks and bonds (I assume your mix of stocks and bonds is in the range I recommend in Chapter X NEC.). And, even though you’ve been withdrawing each year, you still have at least 10% more portfolio value – measured in the same real spending power than you started with. You also have MORE THAN YOU EVER HAD in your life.

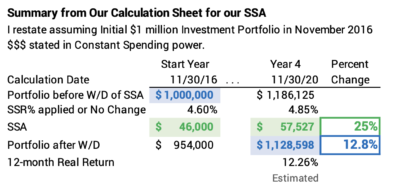

I give a snapshot of the last four years, adjusting our calculation sheet to assume we started our retirement with our first withdrawal for next year’s spending in December 2016. (I’m using results for us for 2020 as of Wednesday, seven days short of the final returns I’ll use as of November 30.) You can see the spreadsheet for the four years here and our calculation sheet last November 30 as reference.

== What’s this mean for the future? ==

We don’t know anything about future returns, but we are in a really good spot now. We can take the view that we have extra – maybe more than we should. We can tweak our spending to create an added a cushion. Here is what I’d consider:

• Set aside some of the money you’ve accumulated in your checking account this year. (I assume you’ve been paying yourself your 2020 SSA steadily throughout the year, and that your checking account is as swollen as Patti’s and mine.) Carry some into 2021 such that you start the year with a big fat amount in your checking account. You’ll be putting pressure on yourself to spend it to Enjoy, and that’s a good thing.

• Don’t withdraw your full SSA for your spending in 2021. If you calculate the same way we do – just after the 12-month period ending November 30 – you’ll calculate to about +10% increase in your SSA for 2021. Base your SSA for 2021 on 95% of your Investment Portfolio, not all of it. In essence, you’re assuming the market is overvalued by 5% and will correct itself.

You’ll increase your SSA, but it will increase by 5% less than you would otherwise calculate. I’d bet you’re not going to miss that extra 5%. You’re giving yourself added cushion and increasing the potential for future increases in your SSA. I’d recalculate each year for sure, like I do the first week in December, to see when you can next increase your SSA. Chances are you’ll see a +15% real increase every four or so years.

I’m leaning to do both: I’m pretty sure we’ll enter into 2021 with a much bigger balance in our checkbook than normal, and I plan on not paying ourselves the full increase I will calculate after November 30.

Conclusion: Covid-19 has been a drag on enjoying life. Everything has been on hold since early March. But good things have happened.

We’ve all slashed spending: we’re down to the basics. We are very clear as to what we want to do to Enjoy More Now and how much that will cost in the future.

Returns for the last two years – more years than that really – mean our financial portfolio is THE BEST IT’S EVER BEEN in our lifetime.

If you are just starting your retirement, you can safely spend ~33% more from your nest egg than you thought you could spend just two years ago.

Those of us who are retired have seen our Safe Spending Amount increase by about 25% over the last four years. We have the ability to create a bit of a cushion for the next year or so: our cushion for 2021 is the cash we haven’t spent from our 2020 SSA, and it is easy for us to pay ourselves less than our full SSA that we’ll calculate for spending in 2021.