What is your benchmark for returns for 2021?

Posted on January 14, 2022

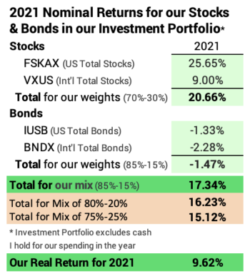

It’s a week or two past the time of year that most of us judge how well our portfolios performed for the past calendar year. This post shows the nominal and real returns Patti and I earned on our portfolio in 2021and over the past seven years from the start of our financial retirement plan. Our nominal return for calendar 2021 was 17.3%. I think that’s a good benchmark for you to use to judge how well you did in 2021. Our real return, adjusting for 7.0% inflation, was 9.6%.

I waited to assemble the returns for our portfolio until the inflation rate for 2021 was released this week. I wanted to get a more accurate picture of the real return rate we earned for the year. I use the Morningstar site to get returns for the year – calendar year returns are posted the day after the last trading day of the year – and this site to get the details on CPI.

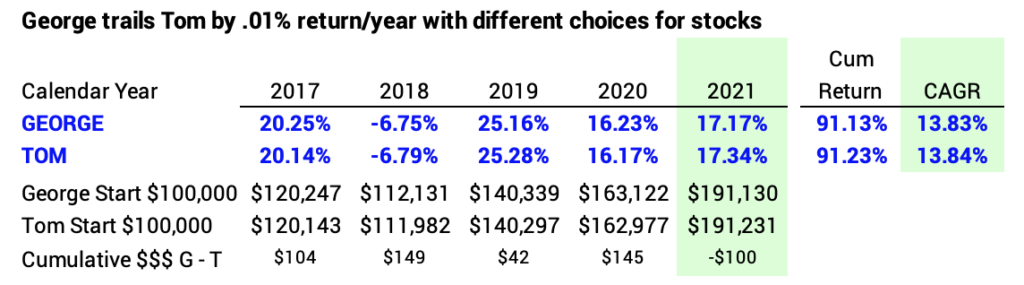

If you hold a similar portfolio – basically index funds – your portfolio return will be similar. My friend, George, and I compare each year. We have the exact same mix of stocks and bonds. He differs because he holds a different US Total Stock fund and a different international stock fund than I do. Over the past five years we differ in average return rate by 0.01%. I’m glad that I’m ahead, otherwise I’d never hear the end of it!

My friend, Fred, has what I consider to be a contorted portfolio of 14 funds designed by his financial advisor. It is not as simple for him to gather all the returns and put them in a spreadsheet to add up and find how his total portfolio return stacks up to 17.3% for our simple, four-fund portfolio. (This likely is something his advisor likes.) I went through the pain to calculate his portfolio return, and I calculate that he lags by three percentage points in return for 2021. He was heavily tilted to small and mid-cap stocks and that was a wrong tilt for 2021. He holds two actively managed technology funds than managed to badly underperform their peer index fund. And that excludes the advisor fees he pays. He also has a lower mix of stocks than I do and that would mean he lags by another point or so.

My guess is that most retired folks, like Fred, lag our 17.4% return by more than two percentage points, and that’s a problem for them. That difference cumulates to A LOT of money over time. A LOT less happiness over time.

You can see our results for the last seven years on this one sheet here.

= My observations ==

Patti and I formally started our retirement plan in December 2014 with our first withdrawal for spending in 2015. It’s been a very good seven years.

• Our portfolio return has been positive for five of the last seven years: both nominal and real returns. Returns in all those five years been greater than the expected return rate for our portfolio. The average real return rate (8.3%) is roughly two percentage points greater than our expected return rate (6.4%).

• Stocks have outperformed bonds by a wide margin – on average by almost 9 percentage points real return per year (9.6% vs. 0.7%). Bonds outperformed stocks in two years, most significantly by 8 percentage points in 2018. This year, the real return for stocks was almost 21 percentage points greater than bonds (12.7% for stocks and -8.0% for bonds).

• The 85% mix of stocks in our portfolio means Patti and I have realized about 14% more happiness over seven years relative to having had a mix of 75% stocks. The greater return meant we calculated to a greater annual Safe Spending Amount and have a larger portfolio now. My view is the 85% is no less risky than 75%, but I have my head and emotion – hopefully – focused on the risk of not having enough to support our spending desires in a future year, not the annual variations in portfolio value.

Conclusion: 2021 was another really good year for stock returns. Not so for bonds. We all have to be happy with 2021 on an absolute scale. Patti and I earned 17.3% on our Investment Portfolio. I think that’s a very good benchmark that you can use to judge your relative results. You should be no lower than 15.1% in total. If your portfolio return is less than this, something is amiss. You should be figuring out how to get closer to an appropriate benchmark of performance for your portfolio.