Did you summarize your 2021 tax return?

Posted on April 15, 2022

Did you summarize your 2021 tax return in a format that is understandable to you? I find the 1040 form confusing. You can spend a bit of time to reorganize it so it’s much easier to understand. The purpose of this post is to provide you two formats that you can use to summarize your 2021 tax return: the short form that I use and one that was in the thick tax return that my accountant sent me. You want to understand your tax return and how decisions you make can avoid taxes that you do not need to pay.

I had two friends tell me they were surprised when they or their accountant completed their tax return. One had a big surprise on the amount of added taxes he had to pay. The other had the pleasant news that she had too much income – money that she will not spend – that was being taxed in the 32% tax bracket: this is is the result of shakey planning; in essence, she will pay excess taxes and not pay her favorite charity.

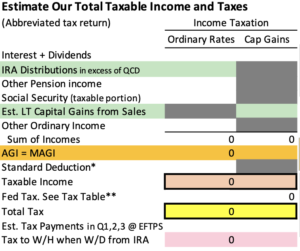

== My short form ==

I make my first real estimate of the taxes I will pay the first week of August each year. I refine it in late November when I decide our Safe Spending Amount (SSA) and the securities I need to sell to get our SSA into cash for the upcoming year. (See Chapters 2 and 9, Nest Egg Care.)

Here is the very simple format that I use to estimate taxes. It’s easy for me to put my details from 2021 in this format as a starting point for 2022. I provided a spreadsheet of this format in this post, and you’ll see it again in August. I’m not looking for precision at this point: I round all numbers to the nearest $50. I show a .pdf of this format with more detail here.

I have three items that I control – to a degree – to minimize the taxes I pay on the total amount of securities I will sell to get our SSA. Two are highlighted in green on the table: 1) I have to sell securities and transfer cash from our IRAs to at least equal RMD for the upcoming year. 2) I have to sell securities in our taxable account, since our SSA is always greater than our RMD; my choice of which securities to sell in our taxable account will affect the amount of taxable gain. 3) Proceeds from sales of securities that I distribute for spending from my Roth account do not appear in my calculation of tax since I previously paid tax when I contributed/converted.

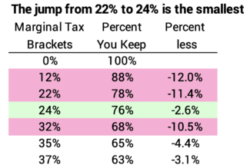

My choices control my Adjusted Gross Income (AGI). That’s the sum of two components of taxable income: the portion that is taxable at ordinary marginal rates and the portion that is taxed at capital gains rates. For the same after-tax proceeds for our spending, I might be able have greater income that is taxed at lower effective capital gains rates and less that is taxed at ordinary marginal tax rates. For the ordinary marginal rate, I don’t sweat the step up in marginal brackets from 22% to 24%; the difference in total taxes paid – or the percentage that you get to keep – is small.

For Patti and me, Adjusted Gross Income is the same as Modified Adjusted Gross Income; we don’t own tax-exempt securities and don’t need to add that income back to AGI to get MAGI. Too much MAGI means you cross an income tripwire that results in greater Medicare Premiums that will be deducted from your gross Social Security benefit. Married folks who had high MAGI on their 2020 return pay more than $10,000/year in added premiums in 2022. High MAGI also determines whether or not you pay an added 3.8% tax on some or all investment income (NIIT).

== Marginal tax brackets ==

One of my friends was confused a bit on the nature of marginal tax brackets. I’m sure you have this: You pay tax at ordinary marginal rates on certain income. You pay flat capital gains rates on certain income – dividends and securities you sell that you’ve held for more than one year. Ordinary rates are graduated, and the marginal tax rate increases as your Ordinary Income increases. The Capital Gains rate is 15% for most all of us; because you are only taxed on the gain, your effective tax rate is low.

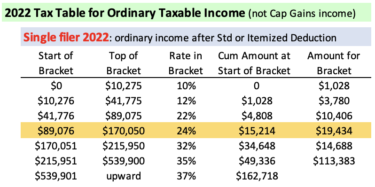

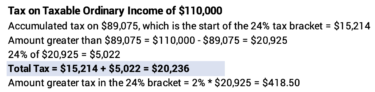

You calculate your tax on ordinary income by using the marginal rate tax table. You first find your applicable bracket. If you are a single filer with taxable ordinary income of $110,000 in 2022, you would be in the 24% tax bracket. (Taxable ordinary income = gross ordinary income less the standard deduction for most all of us.) From the table for 2022 taxes you would pay tax of $15,214 – the tax that cumulated to the start of the bracket – plus 24% of the amount greater than $89,075: total of $20,236 in tax. You pay an added $419 in tax on the increment that fell into the 24% bracket and not the 22% bracket.

== A more detailed sheet ==

I have my tax return prepared by an accountant, and the return copy he sent me contains a much more detailed summary form. I enclose my version of his sheet here. You can pick the items you might add or delete to my short-form sheet to be more applicable to your situation.

Conclusion. You should summarize your 2021 tax return in a format that is easy for you to understand how your Adjusted Gross Income (AGI) is calculated and how much is taxed at ordinary marginal tax rates and how much is taxed at capital gains rates. You have some control over those two components of your tax return and the sum of the two. For most all of us AGI = MAGI. Your MAGI determines Medicare Premiums that you will pay; your MAGI determines whether or not you pay a greater tax on Capital Gains.