Why is it important to rebalance our mix of stocks and bonds in our portfolio?

Posted on October 27, 2017

Annually rebalancing back to our chosen mix of stocks and bonds is far more important for us retirees than it is for younger folks. Rebalancing is “required” when you’re following the CORE principles in Nest Egg Care.

I think many folks who are not retired don’t rebalance their portfolio that often. Nor do they need to in my view for their retirement accounts, in particular. These folks typically have many years before they reach retirement. Their holding period – the length of time they hold an investment before they sell it to obtain cash for spending – is long, maybe 20 years or more.

I recently read the book, The The One-Page Financial Plan, by Carl Richards. I generally liked the book, but I was struck by the statement for one section of the book, “Rebalancing Is the Seventh Wonder of the Investing World.” Richards states that rebalancing your mix of stocks and bonds is “forcing yourself to take money from the thing that did well last year (sell high) and you’re moving it to the area that did less well (buy low).” There’s no further explanation of the effect. Rebalancing sounds nice, but that just doesn’t hang together for me for retirement savings.

When younger folks work through the process of rebalancing for a number of years, they’ll think, “When I rebalance, I’m usually selling stocks to buy bonds. Stocks have greater return potential than bonds. When I rebalance each year for a number of years, I think I’m just lowering my total dollar return. Why am I doing this?”

Good question! The long term real return rate for stocks is about 6.4% and it’s 2.6% for bonds; the rate for stocks is 2.5X that for bonds. (And compounding over many years expands the dollar effect.) It’s hard to argue that you want to hold bonds for long holding periods.

Let’s look at the probabilities and returns for a 20-year holding period. For that period, stocks will outperform bonds about 96% of the time. Also, the worst average annual return rate for stocks is greater than that for bonds (The worst 20-year rate is actually positive for stocks, but negative for bonds.); and over those years the effect of compounding expands the basic 2.5X return advantage.* Holding bonds for that length of time is a “bet” that is on the wrong side of the probabilities and return potential.

Yes, holding a significant portion of bonds smooths out the variability of one-year returns. But younger investors shouldn’t buy into the logic that lower one-year variability of returns is good and therefore pay for that with a low mix of stocks that comes at the expense of a whopping difference in portfolio value in the long run.

I have always had a long-term perspective in my Save and Invest phase. I viewed each annual amount I contributed to my retirement accounts as an investment packet, each with a long holding period – typically more than two decades. Therefore, each of those annual contributions had to be invested in stocks. Therefore, overall I was invested 100% in stocks; I obviously never had to rebalance my retirement portfolio. I tolerated periods of “very bad variability” in stock returns, but I rode through them. (You can read more about my results of just sticking with stocks for one year’s contribution – one investment packet – to my retirement account in a future post.)

Now that I’m retired, it’s completely different. The “game” of Spend and Invest is different from the game of Save and Invest. Once a year I’m selling securities from our nest egg to get cash for next year’s spending. In effect, I’m dissipating our nest egg; I’m not accumulating. My mindset now has to be Remain Worry Free! That’s a BIG SHIFT from the many decades of Save More to Accumulate More!

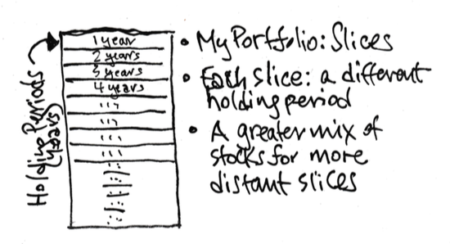

But I stick with one key view of my investments. Just as I viewed each added investment in my retirement account as an investment packet, I now view our total portfolio as a series of spending packets. Each spending packet or slice of the total has a different length of holding period. Some very short. Some very long (hopefully). I’ll consume slices in sequence. We want bonds in many of those spending packets. Why?

We want to hold more bonds for packets with short holding periods. Let’s assume I’ve just sold securities from our investment portfolio for spending over the next 12 months. (Conceptually it’s sitting in my bank checking account.)

The packet that I’ll hold until next year at this time should be almost solely bonds; at most it should have only a splash of stocks. That makes sense from understanding the probabilities and investment returns. For a one-year holding period it’s only somewhat more probable that stocks will outperform bonds. (Stocks beat bonds just 60% of the time for one-year holding periods.) The downside performance of stocks is scary: the worst one-year return for stocks is disgustingly worse (-39% real return) than the worst one-year return for bonds (-11% real return).*

As I think through the slices for future years, more stocks makes sense – the probabilities that stocks outperform bonds improves quickly; the worst performance of stocks is about equal to that of bonds; the compounding of expected return rates makes stocks more attractive. I still want to have bonds in many slices, but at some point the slices should be 100% stocks.

I want to hold bonds, since they’ll keep my emotions in check when “bad variability’ strikes. We’ll be hit (in all probability) with “bad variability” of stock returns in the future. We build our retirement spending and investing plan by assuming we will face horrible sequences returns; that’s what drives our Safe Spending Rate (SSR%) to a low level. I know our SSR% will ensure a long life for our portfolio even in the face of horrible sequences. But when I’m hit with that first instance of “bad variability” of returns my sense of Worry Free may be shaken. The fact that I hold bonds will help. I repeat my “self-talk” speech to prepare me, “Isolate yourself from the emotional stress of ‘bad (possibly disgustingly horrible) variability’ of stock returns, even if that means your portion of bonds means lower total returns over time. You’ll be less stressed and even perhaps happy that you hold bonds in a year when stocks hit the skids and bonds don’t. You’re past the time of life when Accumulate More! was paramount. Now its paramount to Remain Worry Free! Remain Worry Free!”

The decision on mix of stocks and bonds is one of five key decisions for any retirement financial plan. As you work through Nest Egg Care, you’ll make your decision on mix of stocks and bonds from information we get from two Retirement Withdrawal Calculators (RWCs). Mix has two effects on your financial retirement plan. It has an effect on the year-by-year probability of depleting a portfolio for any given spending rate. And it has an effect on the probable value of your portfolio over time. (I’ve done my best in Nest Egg Care to help you understand the tradeoffs of these two effects; you want to engage the “slow thinking” part of your brain on this one!) Therefore, when you’ve completed your Worksheet in Nest Egg Care, your choice of mix is a “strategic” decision. You want to stick with your strategic decisions over time.

The mechanics of RWCs always assume we start each year with the same mix of stocks and bonds. Just to review, an RWC assumes a mix of stocks and bonds (We input that mix.), and the RWC starts every year assuming that design mix. That means it has rebalanced the portfolio to that design mix after it’s withdrawn the chosen constant dollar spending amount for the upcoming year. We’ve got to follow that same process. Rebalance annually.

Conclusion: We retired folks want to hold bonds in our investment portfolio, and we must rebalance our mix of stocks and bonds back to our design mix at the end of each year after we’ve taken our withdrawal for spending in the upcoming year. (Rebalancing is not as simple of a task as I initially thought. It’s much easier if you rebalance at the same time you are selling securities for your spending amount in the upcoming year. You have a spreadsheet in Resources on this site that will help you rebalance annually.)

* See Stocks for the Long Run, Chapter 6, Table 6-1 and Figure 6-1. Jeremy Siegel. Fifth Edition. 2014. McGraw Hill Education. Chapters 5 and 6 are pretty dog-eared in my copy.