Is Rental Property a good income generator for you?

Posted on July 19, 2019

I read this article that suggests Rental Real Estate is a good investment for retirees. I hate even thinking about investing in rental real estate. Or why I’d hold onto it if I had it at this stage in life. This post discusses why I think owning rental property is a really bad idea for us nest eggers.

== Why I don’t like rental Real Estate ==

Oh, let me count the ways!

1. Rental Real Estate is a non-financial asset that can’t consistently give you cash for FUN. Yes, there is modest income that you can spend. But you have most of your money locked up so that you can’t spend to ENJOY. You can’t gift enough to your children’s retirement accounts. You can’t gift enough to your grandchildren’s 529 education plans. Only financial assets consistently give you cash and the potential for more cash for FUN, FAMILY or COMMUNITY while you are alive. I view these non-financial assets largely as a dead weight hanging around your neck.

You want some non-financial assets, though, as a deep, deep reserve to your financial retirement plan, which is fueled by your financial assets. [See Chapter 1, Nest Egg Care (NEC).] My guess is that you already have enough non-financial assets – primarily the equity in your home. You don’t need more.

Most folks I know have TOO MUCH non-financial assets and no HELOC (Home Equity Line of Credit). Because they are overloaded with non-financial assets – or underloaded with financial assets – they are limiting what they can spend on Fun, Family, and Community. Because they have no HELOC, these folks are spending their FUN MONEY on NOT-FUN when the non-financial assets need cash to keep them up to snuff.

2. Rental real estate can’t get close to the potential for increases for your spending. At other than Most Horrible sequences of financial returns, your Safe Spending Amount (SSA) will increase in real terms. (See Part 3, NEC.) Over the first four years of our plan (Patti and me), our SSA has increased by 20%. All nest eggers saw an increase in their SSA over those four years. And the average return rates over the four years were not outta the ballpark by any means. Rental real estate isn’t going to come close to paying you 20% more in four years – that would only come from increasing rents by a real 20% over four years. Your renters would revolt at an increase like that.

3. Rental real estate is painful work. Oh, the headache and hassle: the uncertainty of how long tenants stay; the cash outflow when you aren’t collecting rent; the costs to ready the property for new tenants; the marketing costs to find new tenants; the general and surprise repairs and maintenance; the record keeping. Really, why would anyone ever buy into that? It’s the exact opposite of FUN to me, and this is the time of life to really focus on what’s FUN.

4. You’re hurting your heirs as well as yourself. If you have rental property, sell it and put the proceeds into your financial nest egg.

I am surprised at folks who say, “I’ll hang on to this property because my heirs will get a step up in value when I die; they avoid capital gains taxes that I would otherwise pay.” These folks have the cart before the horse.

My friend, Roy, tells me that he and his wife own a 1,000 square foot house with a lake view. That size might more properly be described as a cabin. His sole, single renter has been there for years and causes no problems; he even paid for the new refrigerator when the old one went kaput. Renting to him has been headache free. Roy hasn’t raised rent much over the years because the tenant has been so good, but Roy has close to no net cash rental income now.

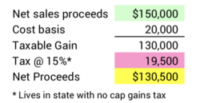

Roy thinks he can net $150,000 from a sale. But he tells me his problem is that his depreciated cost basis is $20,000. His tax preparer told him, “DO NOT SELL!” – or to sell it and reinvest the proceeds in rental real estate again – to avoid paying capital gains taxes in his lifetime. At the death of Roy and his wife, their children get the step up in value. They could sell then and not incur the capital gains taxes that Roy would incur if he sold. Roy and his wife HATE the idea of paying nearly $20,000 in added taxes now, and they conclude their tax preparer is giving them solid advice. Smart guy, I’m sure.

Does that recommendation make sense? NO! This is an example of failing to thoroughly engage the computational part of our brain to compare the two opportunities.

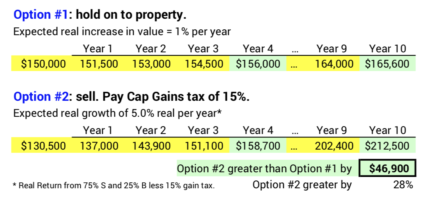

Roy has two options: #1 Not Sell. Hold on to the property or sell it and put the proceeds in similar rental property. His heirs never pay capital gains taxes. #2. Sell. Pay gains tax and put the net proceeds into his financial nest egg. I use expected real returns for his real estate (1% per year) and for his mix of stocks and bond (5% per year after taxes each year). (See here for expected real return rates for stocks and bonds.)

Option #2 wins handily. If he sells, pays tax and invests the proceeds in his mix of stocks and bonds it would take just four years to have more money than his heirs will ever get from the real estate. Roy or his heirs would have nearly $47,000 more money in a decade. (If I had used 2% real growth in value for real estate – highly unlikely in my view – Option #2 pulls ahead in five years, not four.)

This comparison gets ridiculous if I run this out 20 years. Roy’s heirs have than $160,000 more in spending power in 20 years.

== Sell and NO future taxes ==

I personally like this course of action: Sell and Invest the proceeds in 529 plans for the grandchildren. That means NO future capital gains taxes. The grandchildren are very young. The total can compound from a greater mix of stocks than Roy and his wife might want in their retirement portfolio. I calculate this adjustment – the effect of avoiding future taxes on gains – means Option #2 results in $65,000 more in a decade (not $47,000), and that grows to $230,000 more in today’s spending power in 20 years.

Conclusion. Some folks recommend rental real estate as a solid investment for retirees. It’s tough to come up with something that’s worse in my opinion. Non-financial assets can’t come close to your financial assets in providing cash for you to spend to enjoy. They can’t touch the growth potential of financial assets at expected return rates. I suggest you sell rental real estate, pay the gains taxes, and put the net proceeds in your nest egg. My guess is you already have enough non-financial assets – your home. You don’t need more. It’s time for FUN.