Might we all get a real pay increase this year?

Posted on November 8, 2019

Patti and I are +11 months into our performance year for my calculation of our Safe Spending Amount (SSA) for 2020: I use the 12 months from December 1 to November 30. My snapshot in this post tells me that we are just shy of a real pay increase for 2020. If you recalculate your SSA on the same date we do, you probably are just shy of a real pay increase. The purpose of this post is to show how close we – and likely you – are to that real pay increase.

This year is turning out to be better than I thought. Our performance year started with a steep decline in our portfolio in December: -7.6%. At the six-month mark I wrote that it was almost certain we wouldn’t get a real pay increase for 2020. We’d just increase for a Cost of Living Adjustment. (Social Security announced COLA of 1.6% for 2020.) The market moved up sharply from May: +11% for US stocks, for example. All this is to say that Patti and I are close to a real pay increase on top of last year’s SSA + COLA. We need +1 percent return for the rest of November to get us that real pay increase.

== How do you get to a real increase in SSA? ==

You increase your real Safe Spending Amount in a year when returns are good and you have more than enough portfolio value for your current spending rate. You keep the same target year for no chance of depleting your portfolio, but you can do that at a greater real spending rate – you increase your SSA by more than last year + COLA.

You need to use a spreadsheet to track this calculation. We need to inflation-adjust our results to track what is really happening to the spending power of our portfolio. Remember: Think Real. You can see the spreadsheet I have used for the last four years here. The Resources tab on this site’s home page has a spreadsheet you can download to build your calculation sheet.

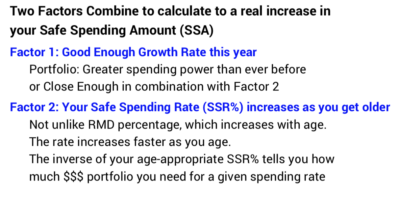

Two factors work together to tell us if we have a real increase in our SSA:

• Factor 1 is a good enough return rate this year. This is the big factor. You obviously have more than enough for your current spending amount when the annual return on your portfolio increases its value to more than its previous high-water mark.

Here’s a simple example. You end 2019 with $1 million portfolio value. You withdraw at SSR% = 4.5% or $45,000 for spending in on 2020. You spend or gift all that. During 2020, the real – inflation adjusted – return on your portfolio is +15%. You earn back the $45,000 that you withdrew and then add about 10% more in real spending power. Right before your next withdrawal at the end of 2020 you have $1,100,000 in the same spending power. If you apply the same 4.5% rate, you can with draw $49,500. You get a real 10% pay increase: $4,500 increase/$45,000.

• Factor 2 is the effect of an increasing Safe Spending Rate (SSR%). This is small factor for younger retirees but it’s a much bigger a factor when we hit our mid-70s and beyond. Because our Safe Spending Rate (SSR%) increases over the years, we actually can fall a little short of the past high-water mark and still get a real pay increase. Stated differently: as the years pass, we need less real portfolio value for the same real spending amount.

Our SSR% increases because our life expectancy is fewer and fewer years. [This why RMD percentages increases each year.] We nest eggers logically plan to the same year of no chance of depleting our portfolio – but it’s about one year less than this time last year.

Here’s a simple example. You end 2019 with $1 million portfolio value. You withdraw SSR% = 4.5% or $45,000 for spending for 2020. The 4.5% rate means you have 18 years for no chance of depleting your portfolio – to the end of 2037. (See Chapter 2 and Appendix D, Nest Egg Care.) You spend or gift all the $45,000. During 2020 you’re real return earn back the $45,000 that you withdrew. Right before your next withdrawal you have the same $1 million in spending power. Your age-appropriate SSR% at the end of 2020 is now 4.6%: that still gives to the end of 2037 for no chance of depleting your portfolio. You apply that 4.6% rate to the $1 million and withdraw $46,000. You get a +2% real pay increase: $1,000 increase/$45,000.

You can read more on this is Chapter 7, Nest Egg Care. I also described how these two factors combined for our 15% real increase in SSA in December 2017.

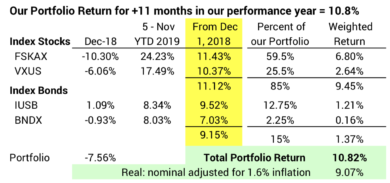

== Our portfolio return rate for +11 months is ~11% ==

Our portfolio has grown in dollars by 10.8% from December 1 through November 5. that’s a real return of 9.1% when I adjust for inflation. That rate is the combination of the horrible return in December 2018 and the very good 2019 Year-To-Date returns.

You can see that bond returns are close to stock returns. That means total portfolio returns don’t vary much over a range of mix of stocks vs. bonds.

The 9.1% real return isn’t enough to get us to the previous high-water mark of portfolio value. We didn’t just have to surpass the portfolio value on November 30, 2018. That wasn’t the high-water mark. We had to beat the value on November 30, 2017. Patti and I withdrew about 4.8% that December for our spending in 2018; the real return for that year was -1.7%; and last December we withdrew about 4.8% for our spending this year. Those add up to more than -9.1%.

Our age-appropriate SSR% has increased since December 2017, meaning we don’t quite have to reach the prior high-water mark. But that’s not helping enough. The two factors don’t combine to a greater real SSA.

I can plug in return rates in my calculation spreadsheet and find the return rate that would give us a real pay increase. We need a nominal return of at least 12% – a real return that’s a shade over 10% – for the 12 months ending this November 30. That’s about one percentage point more than we have now. If the return for the balance of November is +1%, we’ll pay ourselves a real increase for spending in 2020.

== Your math may work out better ==

My guess is that you are younger than Patti (72): her age and life expectancy determine our age-appropriate SSR%. That means your SSR% has been lower; you’ve been taking less from your portfolio. You need less return to get back to your high-water mark of November 30, 2017. That 10.8% return alone could get you to a new high-water mark.

Conclusion. Returns for the first +11 months of our performance year are good: +11% on our portfolio. That’s not enough for us to calculate to a real increase in our Safe Spending Amount for 2020. We need a return rate that overcomes the withdrawal in December 2017, the negative real return in 2018, and the withdrawal in December 2018. +11% just doesn’t quite do that. If we gain 1% more by the end of this month, we will have enough for a real pay increase in 2020. That would be the third real pay increase in the first five recalculations of our plan.